Equities opened strong on Monday as crude oil topped $70 a barrel. Oil stocks and crude oil gave back some of the gains as investors anticipate President Trump’s decision on sanctions on Iran. Oil prices may peak in the next day or two as the market has largely priced in the move.

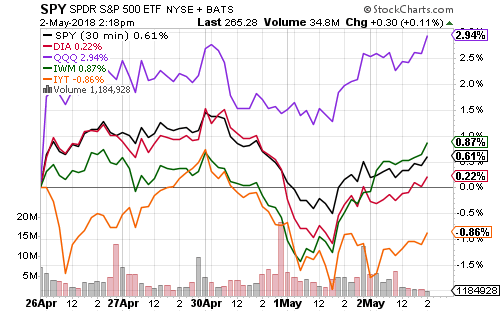

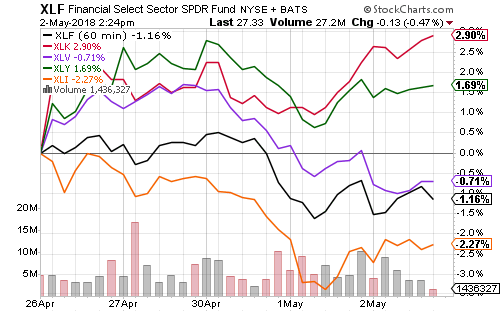

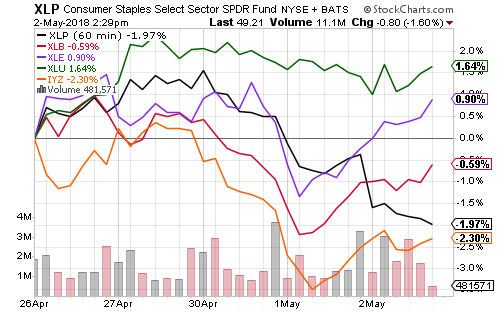

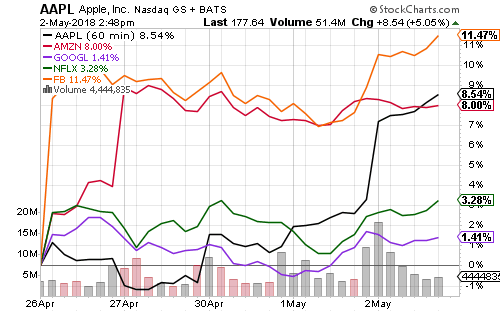

Technology, financials and industrials were the strongest sectors on Monday. Utilities and consumer staples were the weakest. AI and cryptocurrency chipmaker Nvidia (NVDA) rallied near its all-time high on Monday ahead of earnings later this week. Apple hit a new all-time high and its market capitalization crossed $900 billion.

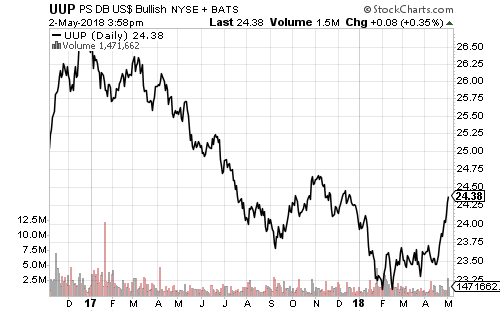

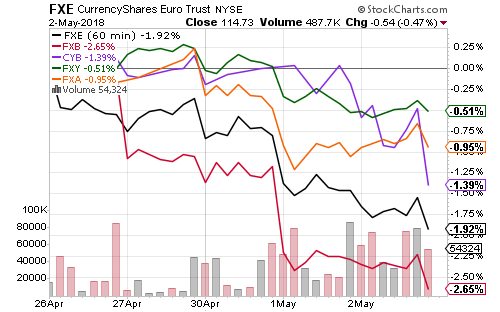

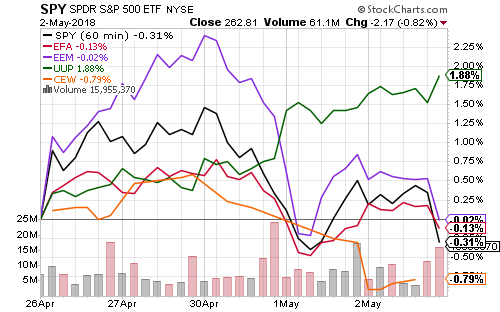

The U.S. dollar extended its rally on Monday as well. WisdomTree Emerging Market Currency (CEW) broke below its rising trend line (going back to January 2016) on Monday, as did iShares MSCI Emerging Market (EEM).

This week will be light on economic reports. Tuesday will bring April small business confidence. April producer prices will be out on Wednesday, and the consumer price index on Thursday. The University of Michigan will put out its advance reading of May consumer sentiment on Friday.

Chinese April trade, new loans, and inflation data will be out early this week. Last week, South Korean trade declined for the first time since 2016. Copper, a key industrial commodity for the Chinese economy, is also headed for a “death cross” this week as the 50-day moving average falls below 200-day.

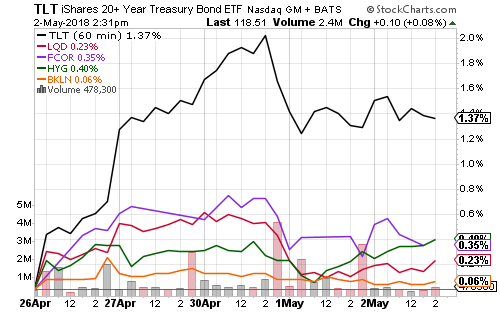

The 10-year Treasury yield started the week at 2.96 percent. It is still consolidating after hitting a new 52-week high of 3.04 percent in April. Many technical traders are waiting for a break of 3.05 percent, but the market also remains heavily short, increasing the potential for a short-squeeze that takes rates lower in the near term.

Ten-year U.S. treasury bonds yielded 2.4 percent more than Germany 10-year government bonds today, the widest spread since the 1980s. While this spread has steadily widened since August 2017, the dollar only began its major breakout versus the euro last month. The last time the spread was this wide, the U.S. Dollar Index was over 100 and the euro was at $1.05 versus $1.20 today.

Earnings season is now 80 percent complete, but several blue-chip companies will report this week including Disney (DIS), Anheuser-Busch (BUD), Nvidia (NVDA) and Duke Energy (DUK). Sysco (SYY), Nutrien (NTR), Tyson Foods (TSN), and Occidental Petroleum (OXY) will also report.