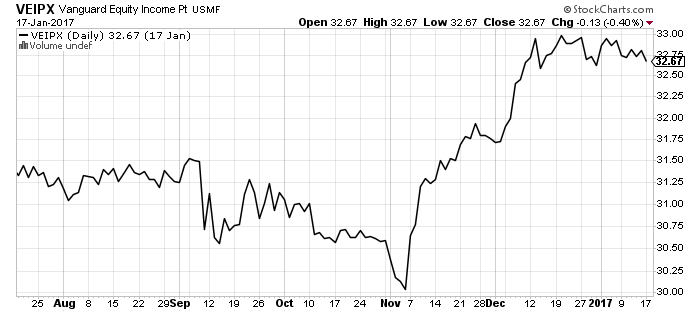

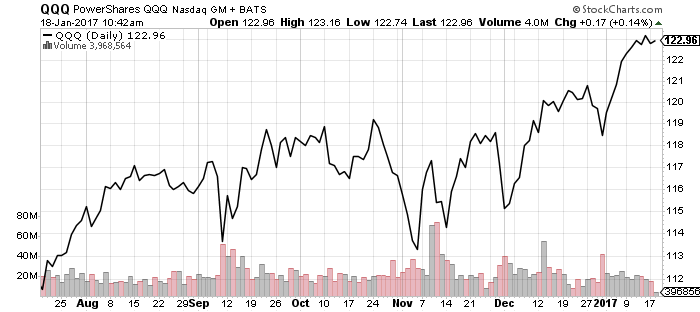

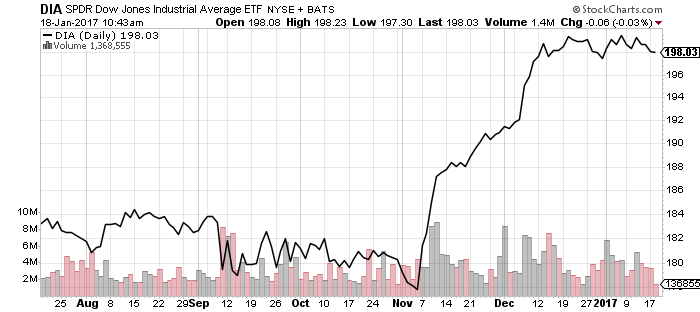

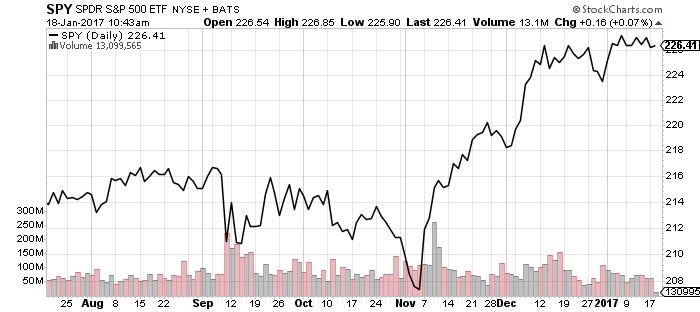

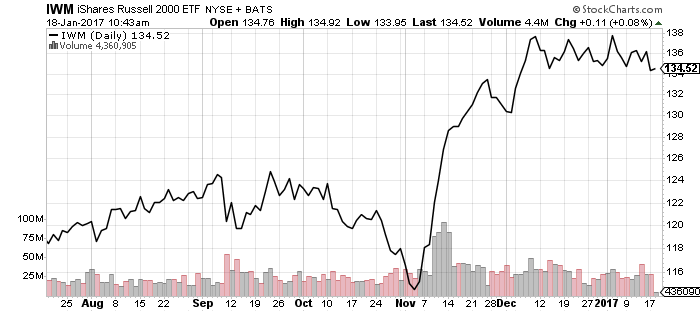

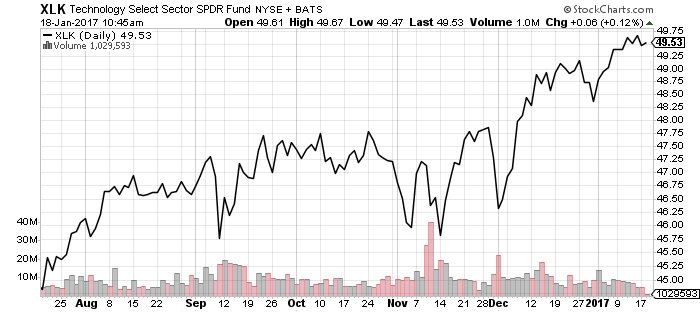

The Nasdaq hit a new all-time high over the past week, while the Dow Jones Industrial Average and Russell 2000 are in a trading range, consolidating early December gains.

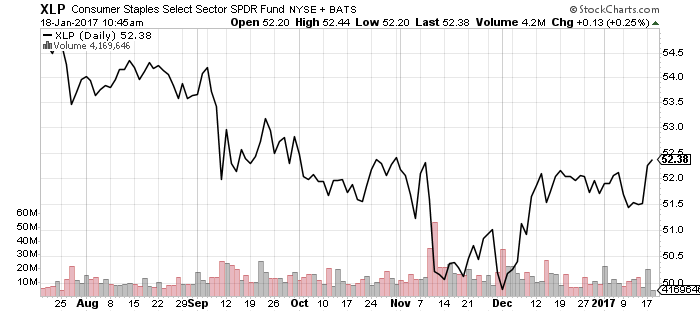

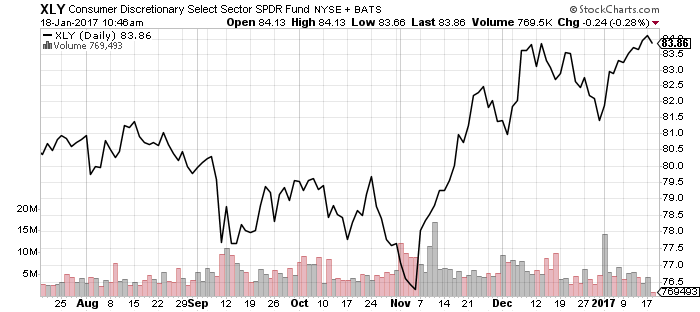

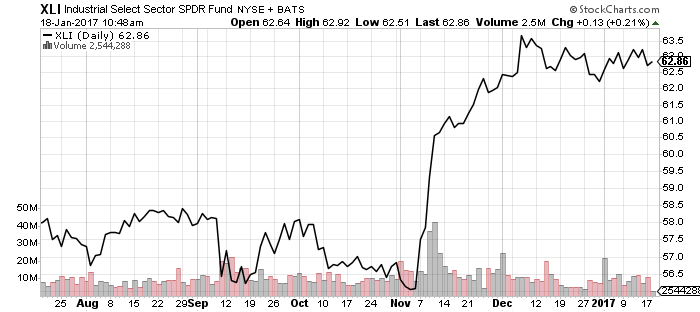

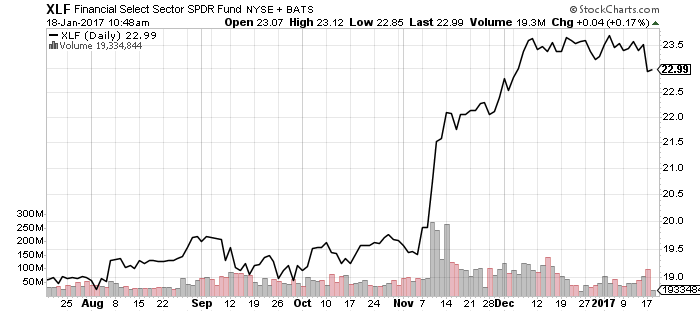

Technology has driven most of the Nasdaq’s outperformance. Consumer discretionary, also weighted heavily in the Nasdaq at 21 percent of assets, pushed to a new high over the past week. Consumer staples rebounded strongly as interest rates pulled back. Industrials and financials, which led the post-election rally, remain in consolidation.

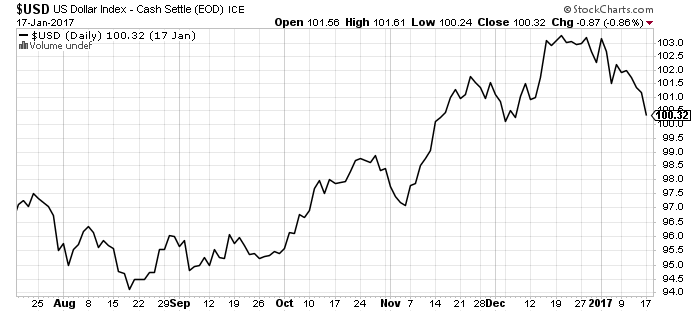

Financial companies broadly surpassed earnings estimates over the past week. J.P. Morgan (JPM) and Bank of America (BAC) exceeded expectations last week, and Morgan Stanley (MS) beat on Tuesday. On Wednesday morning, both Goldman Sachs (GS) and Citigroup (C) also beat earnings estimates. Instead of tracking with earnings reports, however, XLF tracked with the U.S. dollar, which fell 1 percent on Tuesday and then bounced higher on Wednesday.

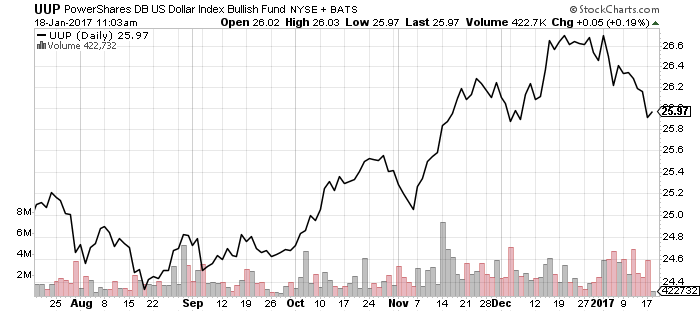

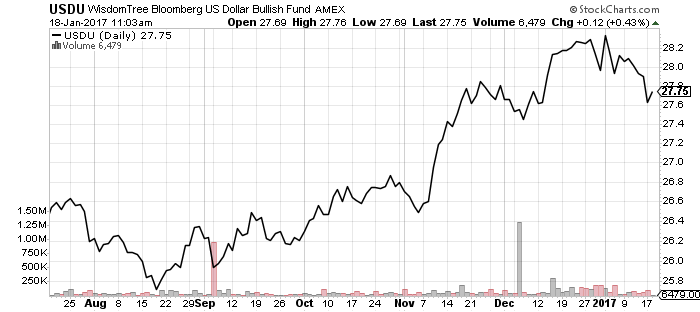

Last week we speculated that a drop below 101 would threaten the short-term bullish trend in the dollar, and it did fall on Tuesday. A dip below 100 is now possible. If historical trends hold true, a correction to around 97 on the U.S. Dollar Index is possible over the next three months.

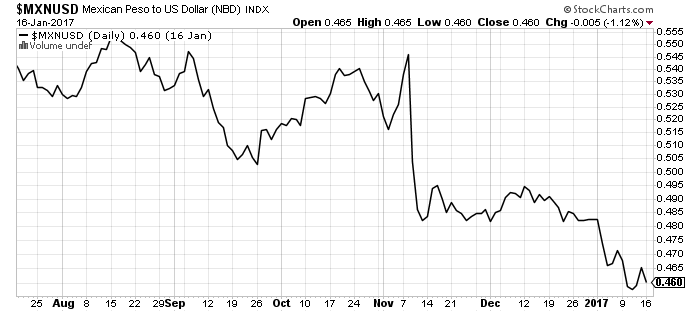

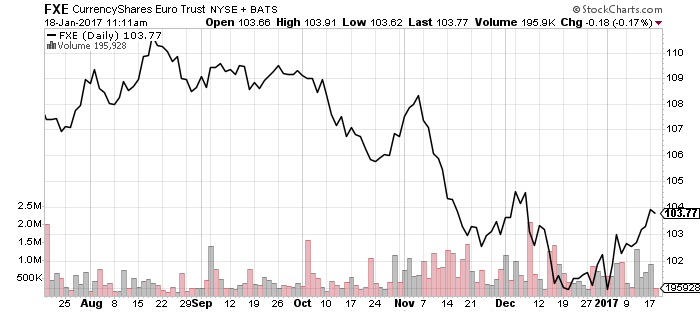

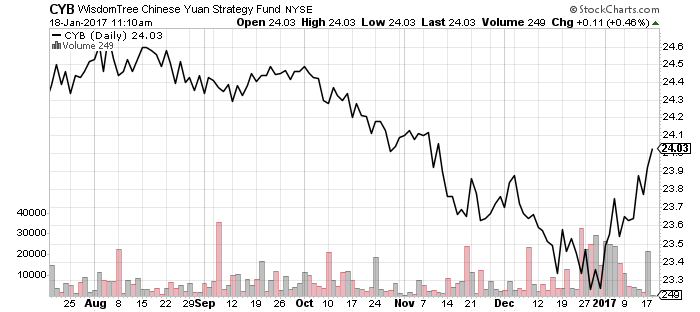

The euro and Chinese yuan have rallied versus the dollar in 2017. The Mexican peso has struggled as speculators contemplate the new U.S. administration. Aside from changes in trade, Mexico receives a large flow of remittances from illegal aliens working in the USA. A border wall and enforcement of immigration laws could have a meaningful impact on Mexican GDP.

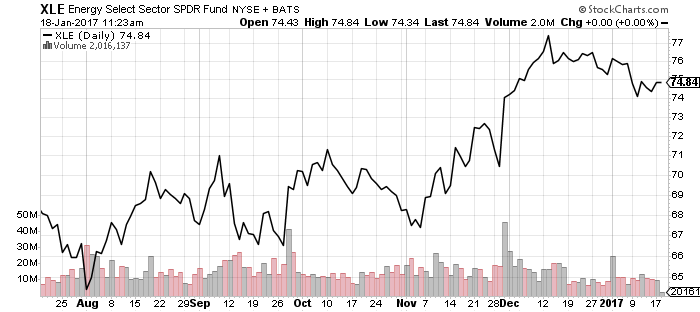

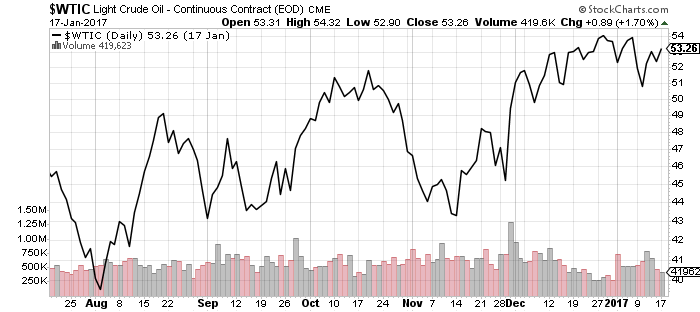

Although a weaker U.S. dollar could help energy in the short-term, the production cut deal could terminate early. Saudi Arabia alleged it will have cleared oversupply by mid-2017. If energy demand remains stable, however, the end of the deal would lead to higher production and lower prices in the second half of the year.

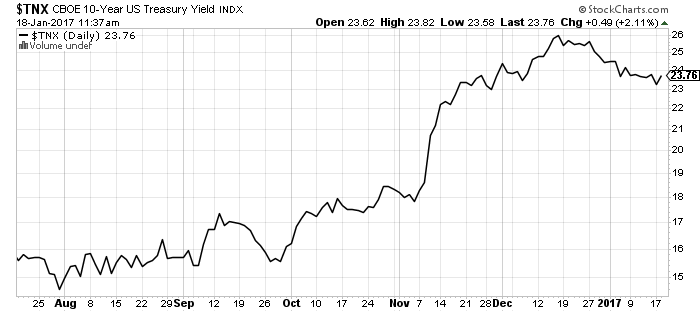

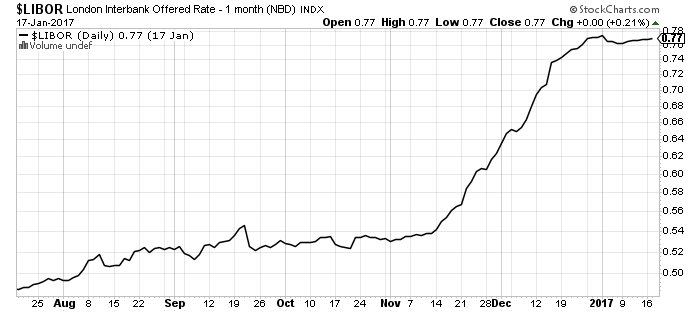

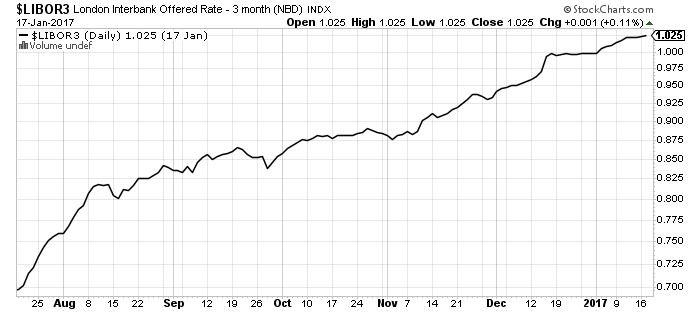

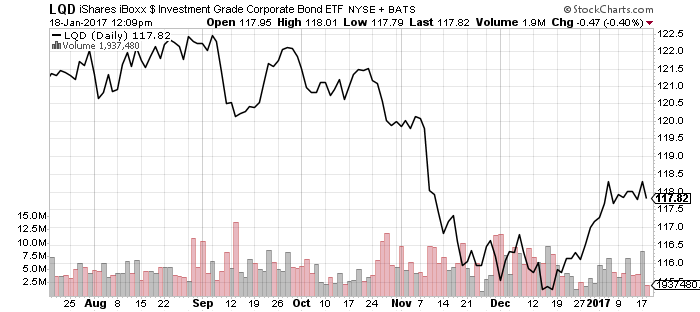

Interest rates mirror the broader stock market’s consolidation pattern. Three-month LIBOR points to rising rates in the near term, while LIBOR is holding steady after the Federal Reserve’s December hike. At 0.77 percent, LIBOR is slightly above the Fed’s interest rate range of 0.50 to 0.75 percent. The Fed indicated three rate hikes in 2017 are possible, but the markets remain skeptical.

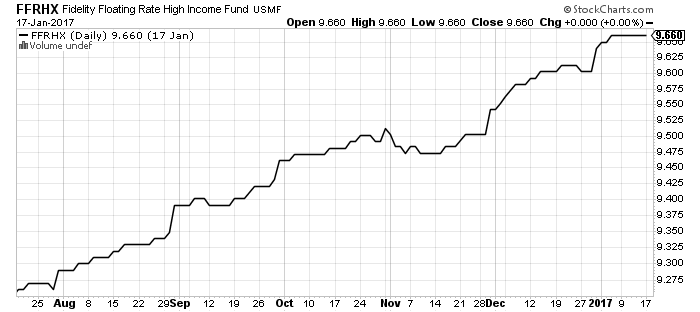

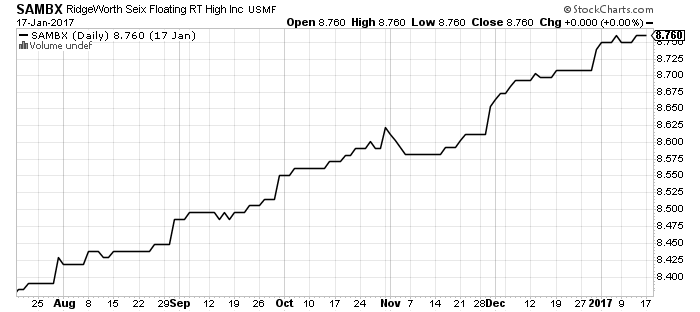

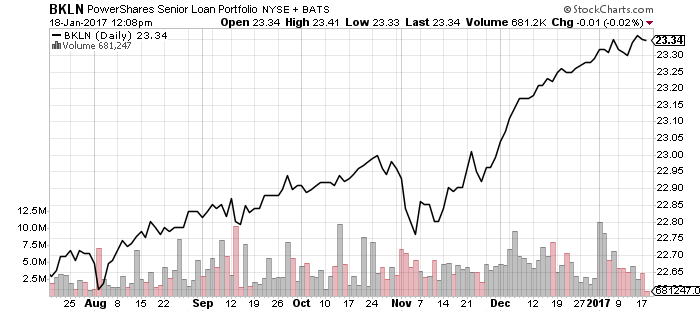

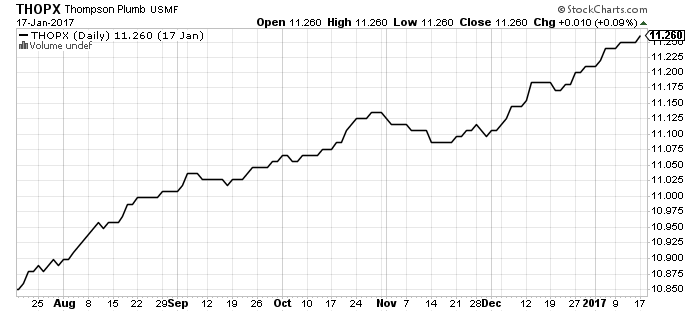

Fidelity Floating Rate High Income (FFRHX), PowerShares Senior Loan (BKLN) and RidgeWorth Seix Floating Rate High Income (SAMBX) are still holding steady or edging higher. Thompson Bond (THOPX) remains in the sweet spot of the bond market.

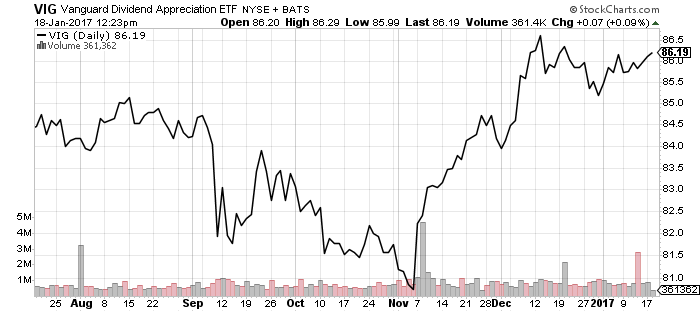

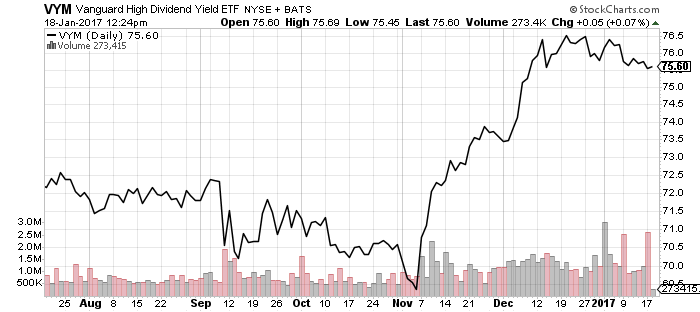

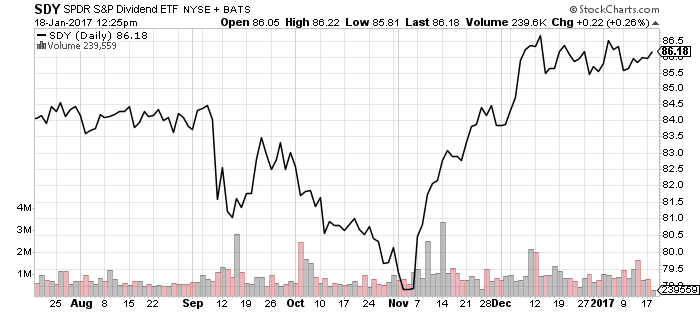

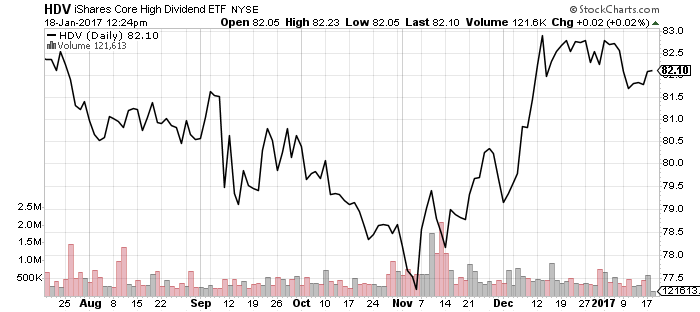

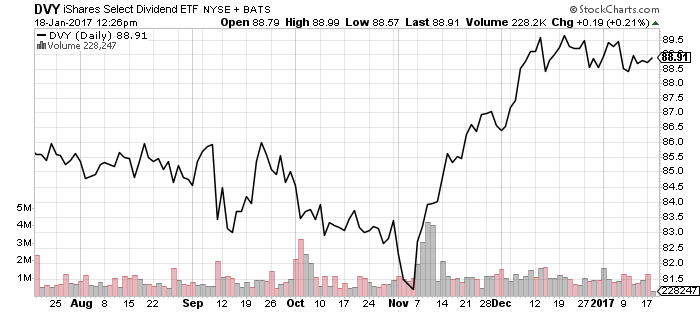

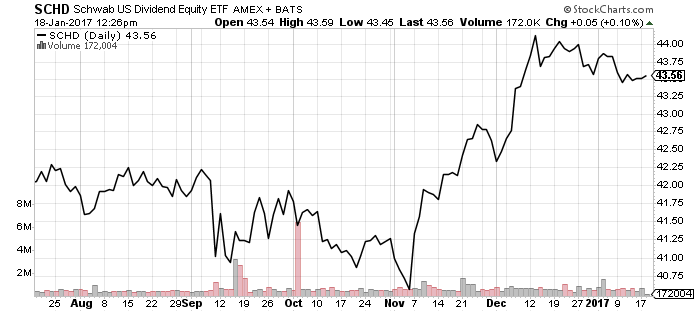

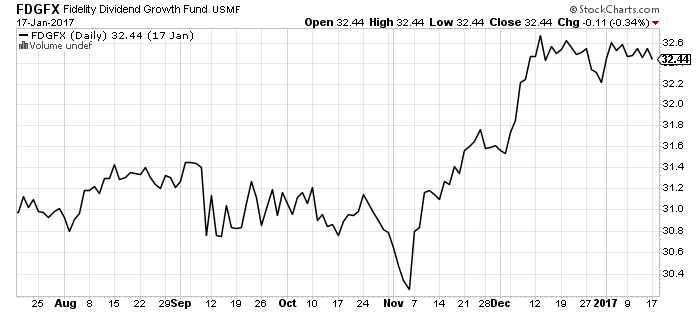

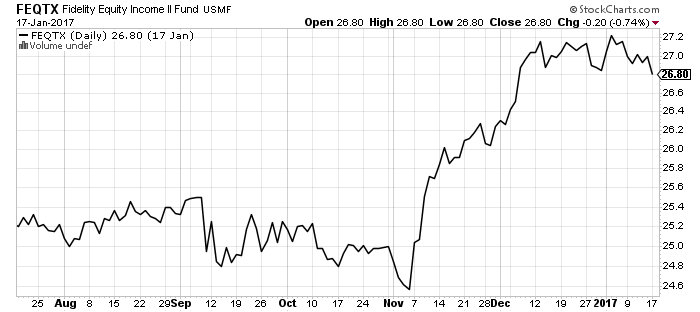

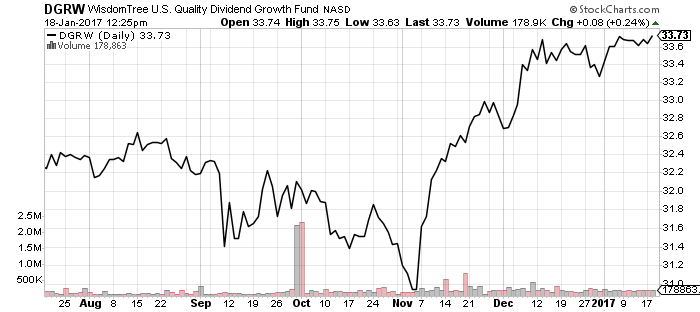

WisdomTree U.S. Quality Dividend Growth (DGRW) has outperformed other dividend funds due to healthcare and technology exposure.