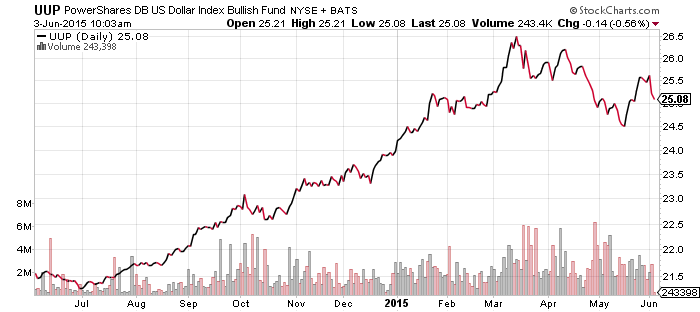

PowerShares U.S. Dollar Index Bullish Fund (UUP)

CurrencyShares Euro Trust (FXE)

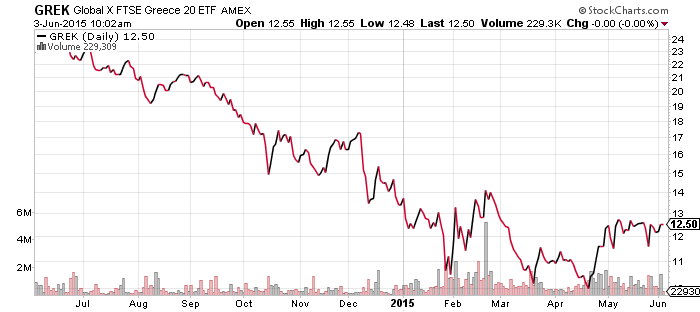

Global X FTSE Greece 20 (GREK)

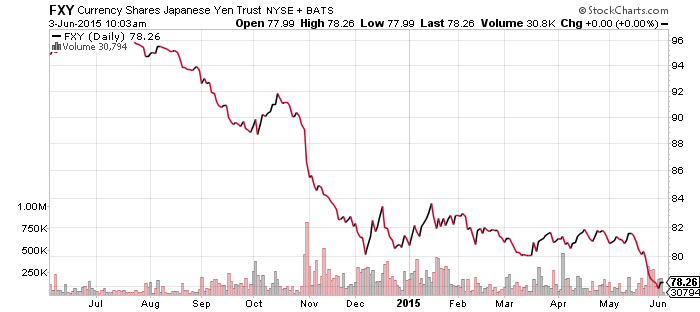

CurrencyShares Japanese Yen (FXY)

We’ve recommended watching the euro to get the inside scoop on Greek debt negotiations. On Tuesday, the euro spiked higher on no news, signaling there was probably a rough agreement behind the scenes. As of this morning, there were rumors of a compromise deal crafted by the Troika, but the Greek government denied it had agreed to anything, let alone received a formal offer.

Assuming a deal is realized, we’ll finally get a clean signal on the euro and by extension, get some insight into whether the U.S. dollar bull market is over or ready to challenge previous highs. Greece only became a significant problem in December and the subsequent sharp drop in the euro accelerated an existing trend. The rebound from recent lows hasn’t yet brought the euro back to that trendline. Even with a deal, the European Central Bank’s quantitative easing program and expectations of interest rate hikes by the Federal Reserve, plus other fundamental factors such as increased U.S. oil production reducing the trade deficit, are still working to lift the U.S. dollar against foreign currencies.

As for the yen, it broke lower last week, but technical traders are still looking for the yen to reverse course. In the past couple of years, these breakdowns have quickly led to a plunge in the yen. With many traders still expecting the yen to rebound, a further break to the downside would catch many traders on the wrong side of the trade, providing the fuel for another big drop.

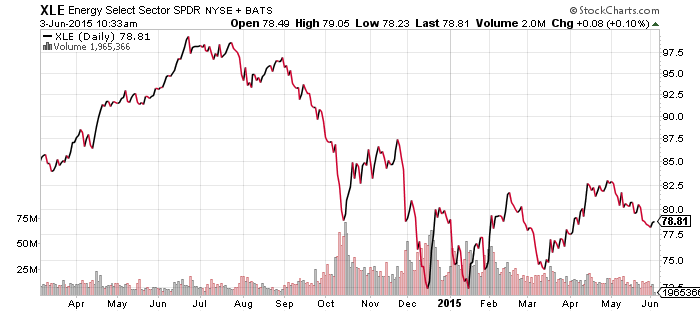

SPDR Energy (XLE)

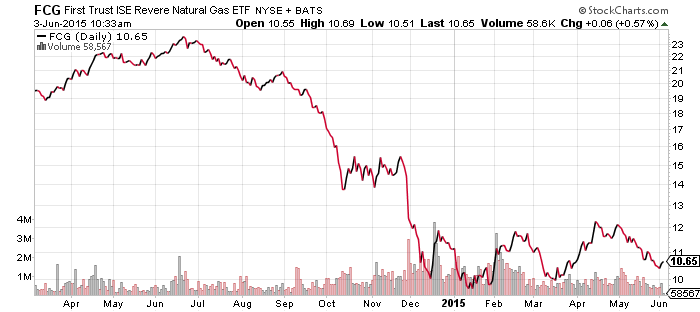

FirstTrust ISE Revere Natural Gas (FCG)

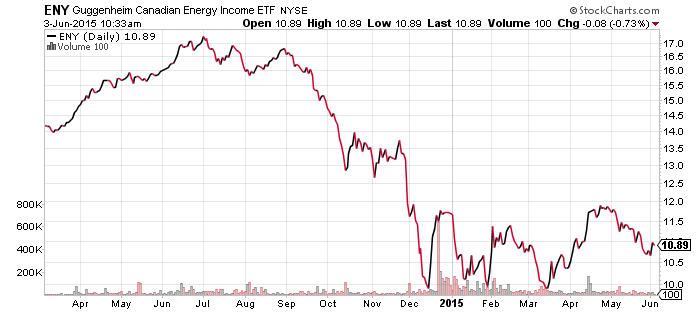

Guggenheim Canadian Energy Income (ENY)

Market Vectors Russia (RSX)

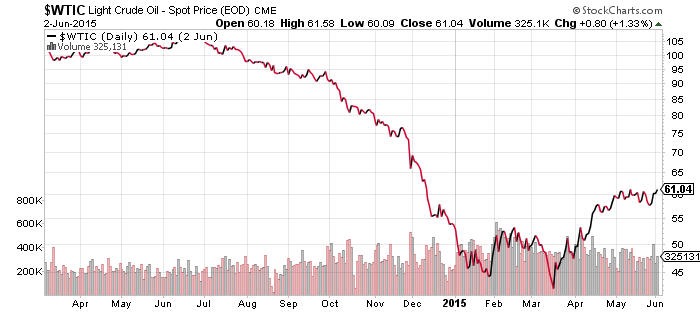

Oil prices edged higher last week. A further move to the upside could be very bullish for the sector because there’s little resistance in the $60s and low $70s. The price of oil is still below the intraday high set in early May though, so this is not yet a breakout.

Shares of RSX slipped today due to a drop in the ruble as Ukrainian separatists resumed their attacks.

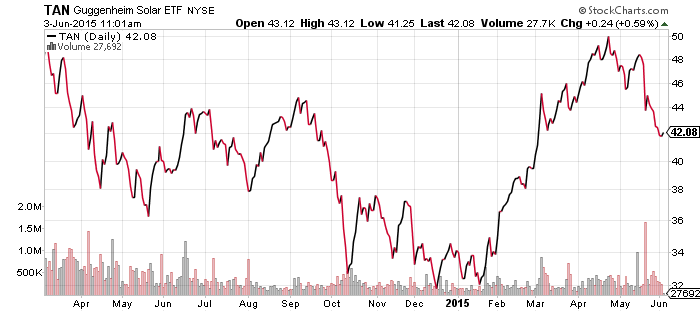

Guggenheim Solar (TAN)

Hanergy is still in TAN’s portfolio because it hasn’t resumed trading. Investors are trying to figure out if Hanergy has engaged in financial shenanigans, if not fraud and stock manipulation. At this point, the firm is still a bit of a black box and shares are unlikely to resume trading until more is known. Shares continue to trade in the U.S. over the counter market but at a nearly 40 percent discount. TAN is pricing the shares at that price because Hanergy was about 6 percent of the portfolio after the first plunge, and now it is about 3 percent of the portfolio. That still leaves room for more losses, though it is likely any further drop will be modest. Even if Hanergy goes to zero, it would only knock $1.20 off TAN’s value, which while negative, is not a large amount for this very volatile fund. There’s also the possibility that concerns are overblown and Hangery recovers.

SPDR Utilities (XLU)

SPDR Pharmaceuticals (XPH)

SPDR Materials (XLB)

SPDR Consumer Staples (XLP)

SPDR Consumer Discretionary (XLY)

SPDR Healthcare (XLV)

SPDR Technology (XLK)

SPDR Financials (XLF)

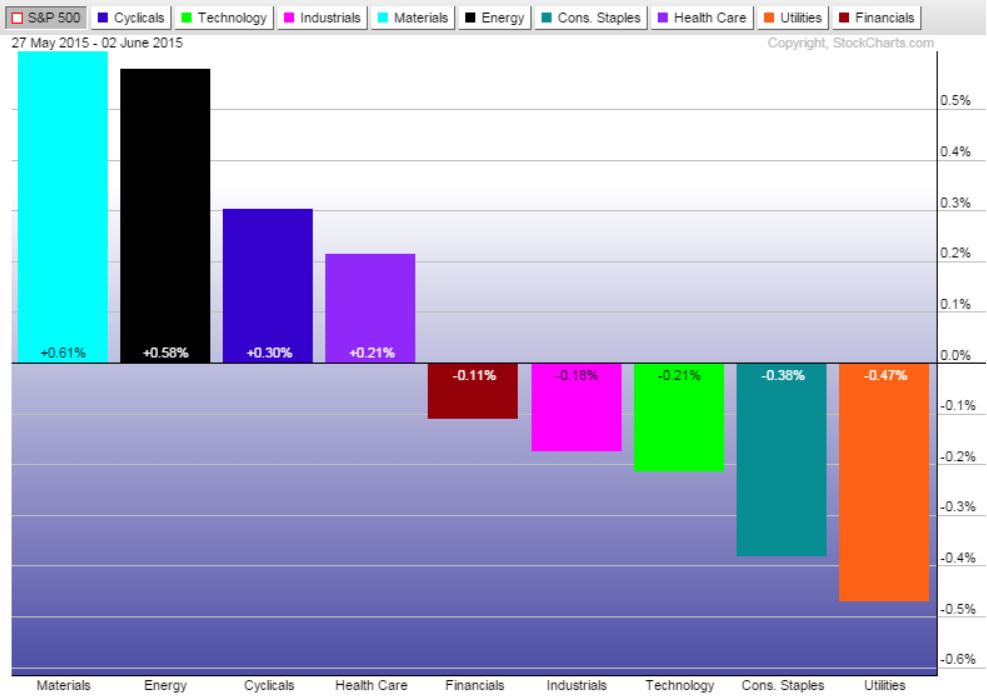

The chart below shows how each sector performed relative to the S&P 500 Index. Materials and energy were the winners thanks to the drop in the U.S. dollar on Tuesday.

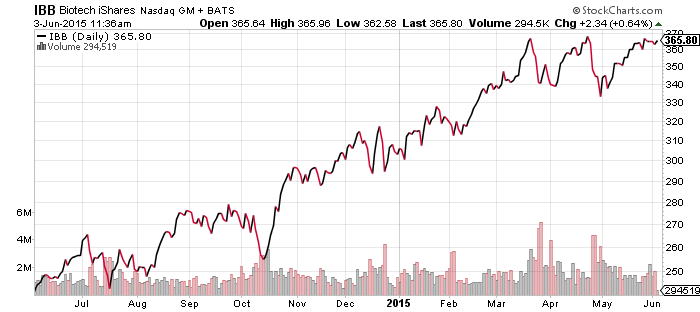

Biotechnology has broken out to a new high if we measure by the small-cap dominated XBI. The large cap IBB has yet to follow, but is likely to rally this week.

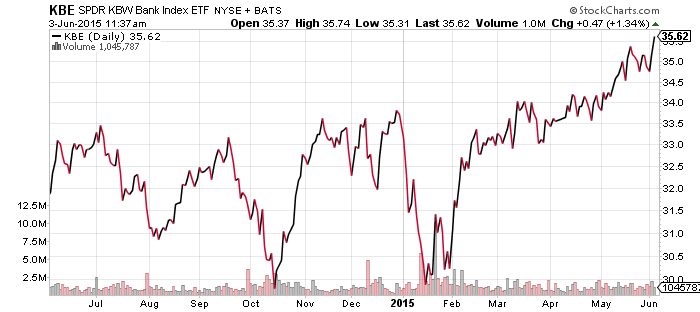

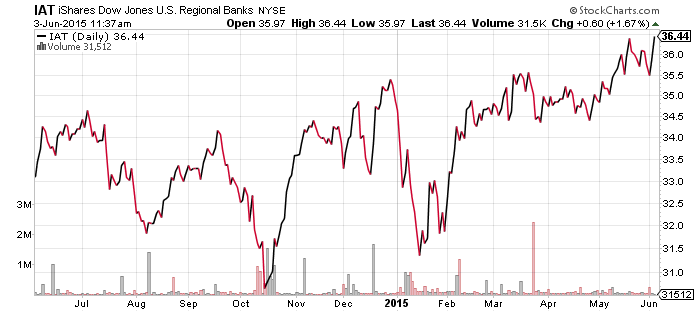

Bank shares are breaking out as interest rates rise. KBE has hit a new high and this signals a bullish breakout for the banking sector. IAT is lagging a bit, but it too should rally over the coming days.

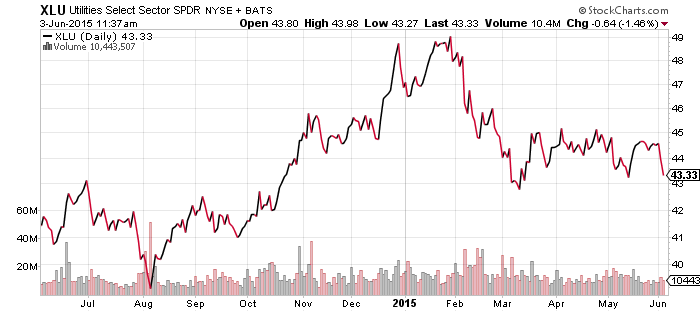

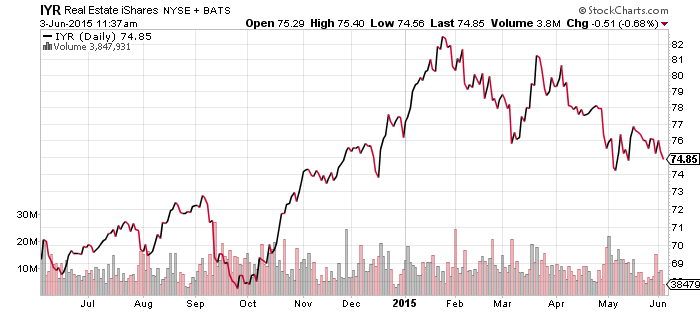

Rate sensitive real estate and utilities continue to slump.

SPDR S&P 500 Large Cap Value (SPYV)

SPDR S&P 500 Large Cap Growth (SPYG)

Energy remains a weight on the value sector, but the improvement in financials may cement a change in trend that favors value over growth.

SPDR S&P 500 (SPY)

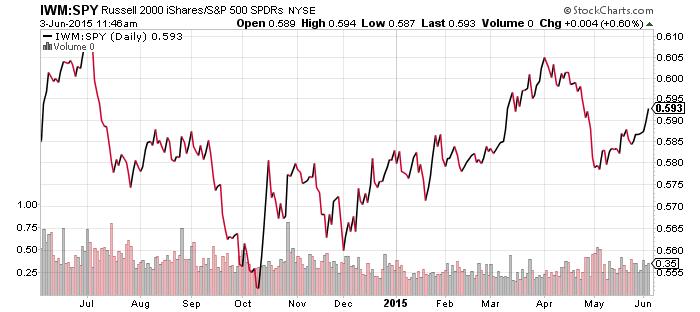

iShares Russell 2000 (IWM)

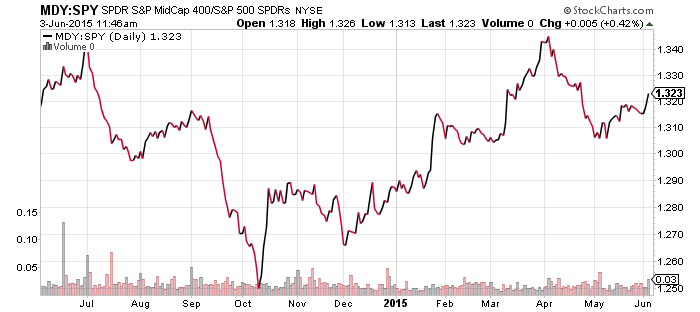

S&P Midcap 400 (MDY)

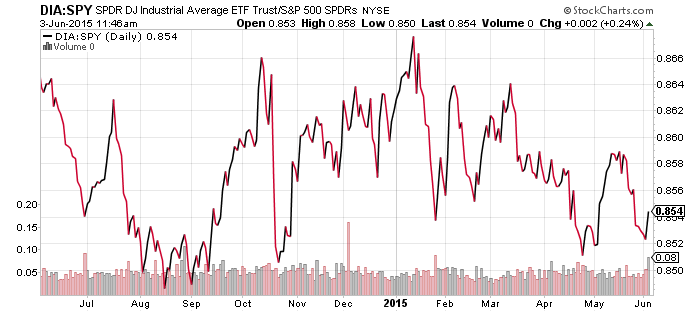

SPDR DJIA (DIA)

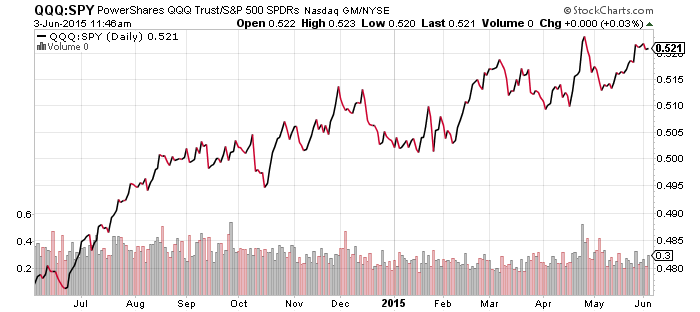

PowerShares QQQ (QQQ)

Small-caps are starting to outperform the broader market and they’re also pulling ahead of mid-caps. The Dow Jones Industrial Average continues to lag the S&P 500 Index, while the technology laden Nasdaq remains the leader in 2015.

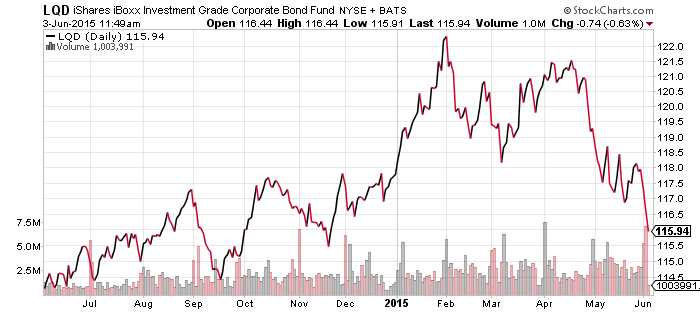

iShares iBoxx Investment Grade Corporate Bond (LQD)

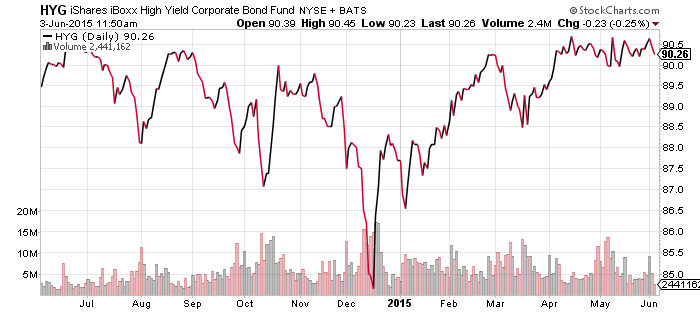

iShares iBoxx High Yield Corporate Bond (HYG)

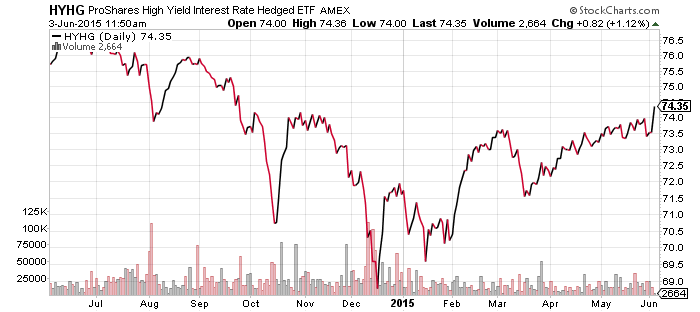

ProShares High Yield Rate Hedged (HYHG)

Interest rates are rising and bonds with longer durations are being hit hard. LQD is down 5 percent from its February high, including dividends. HYG has done much better, holding its value in the face of rising rates. Thanks to its short position in Treasury bonds, the rate hedged HYHG is thriving as interest rates rally.

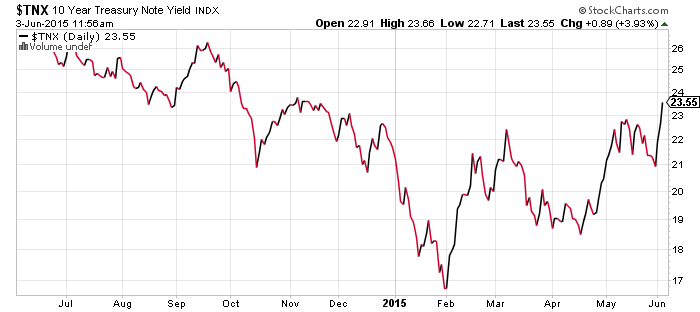

Bond yields are rising globally and the 10-year treasury yield is close to making a short-term bullish breakout. Over the past two days, the drop in German government bonds has been the biggest move since 1998. Concern about Greece may be adding to volatility, but if this move in rates represents a larger shift in bond markets, global financial markets will start experiencing volatility.