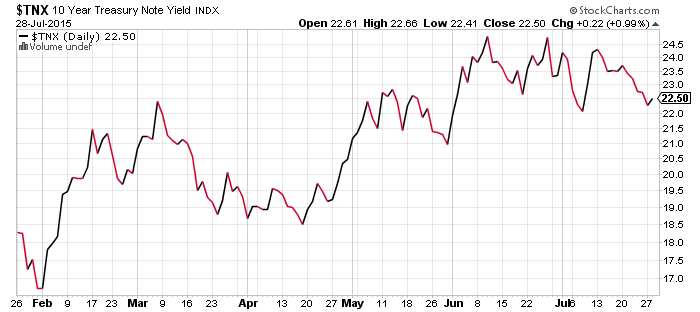

Today the Federal Reserve will put out its latest policy statement. The Fed funds futures market has been remarkably calm since mid-July and a hike by December is a certainty, the market is unsure if it will occur in September. The last comments by a Fed official, made by Federal Reserve Bank President Bullard, put a September hike at 50/50. There are basically three likely outcomes based on investor expectations that the Federal Reserve will telegraph a change at least one meeting early.

The dovish outcome: the Fed does not change its policy statement. A September rate hike will not occur and investors who have said the Fed won’t hike rates in 2015 will be emboldened. Stocks would likely rally on this news, interest rates would decline and the dollar would fall.

The neutral outcome: the Fed changes the policy statement to allow for a rate hike in September or any subsequent meeting.

The hawkish outcome: the Fed statement signals a September rate hike is coming, giving investors two months to adjust. This could also open the door to a second rate hike in December. Interest rates would rise, financials and the U.S. dollar should rally and commodities would likely drop.

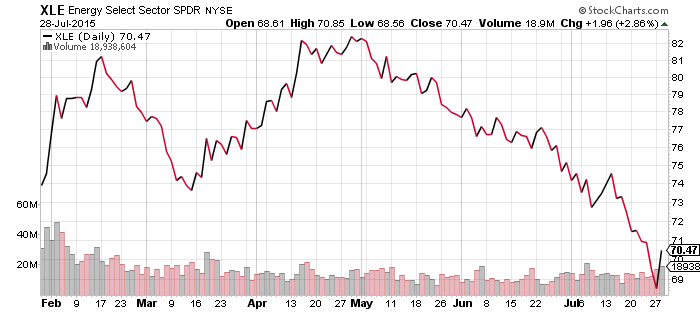

SPDR Energy (XLE)

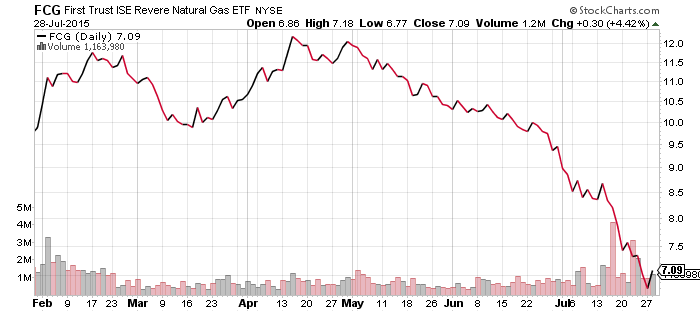

FirstTrust ISE Revere Natural Gas (FCG)

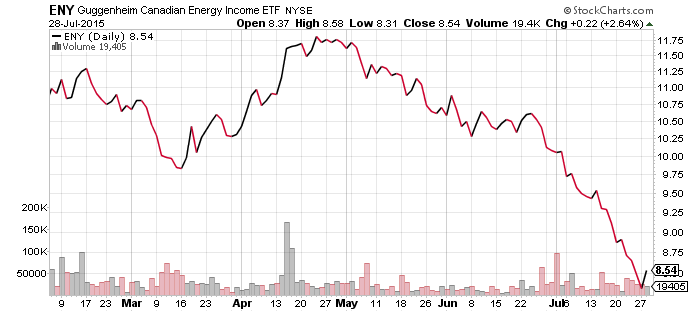

Guggenheim Canadian Energy Income (ENY)

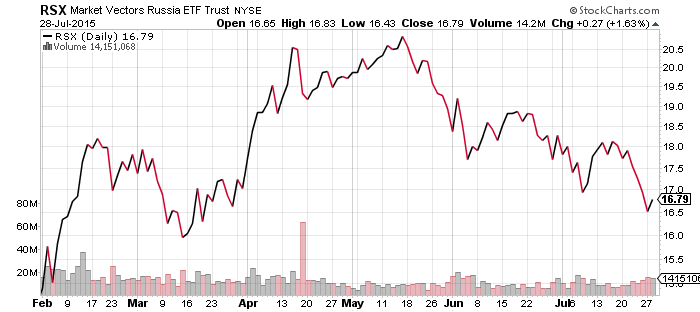

Market Vectors Russia (RSX)

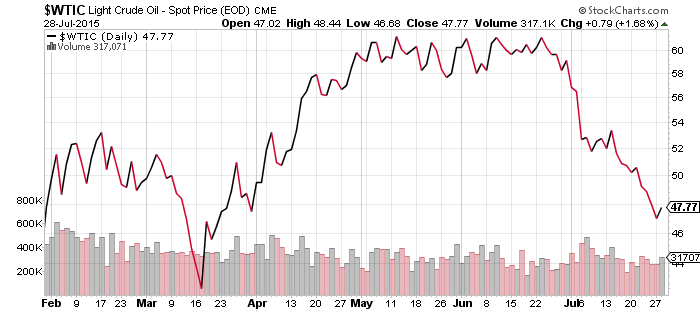

West Texas Intermediate Crude fell below the $50 level last week. Oil prices are currently oversold and a bounce is likely if prices can firm. The pace of the decline has started to slow in the past week, which is good news.

Equity investors tend to lead the energy market. They started selling energy stocks in May when oil prices stopped rising. The recent spike in energy could be the beginning of a rally, but it is important to remember a rally attempt failed earlier this month.

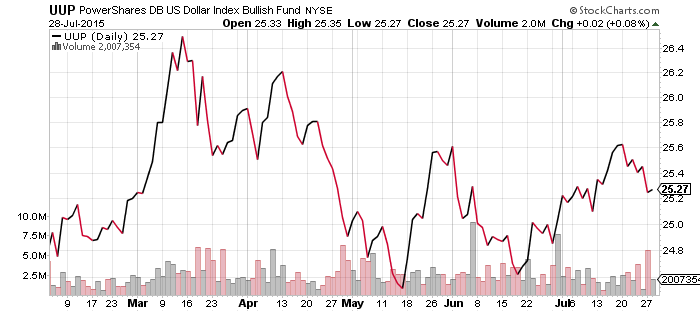

PowerShares U.S. Dollar Index Bullish Fund (UUP)

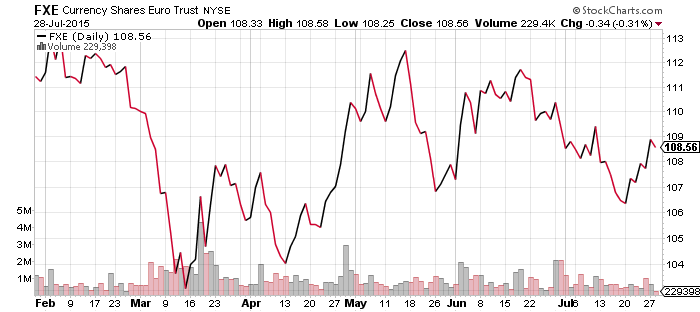

CurrencyShares Euro Trust (FXE)

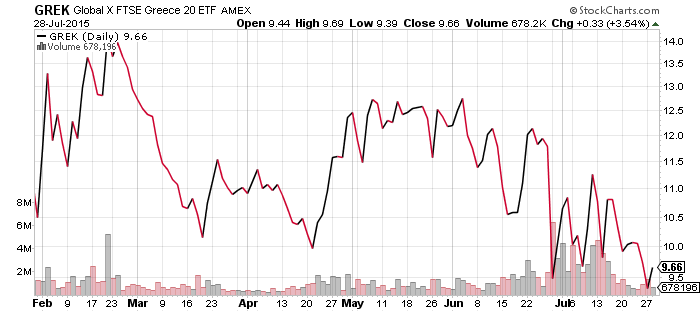

Global X FTSE Greece 20 (GREK)

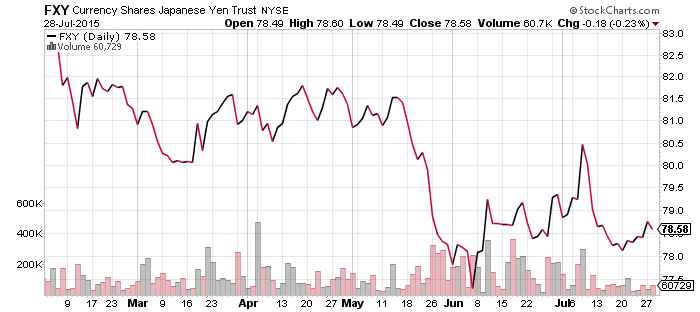

CurrencyShares Japanese Yen (FXY)

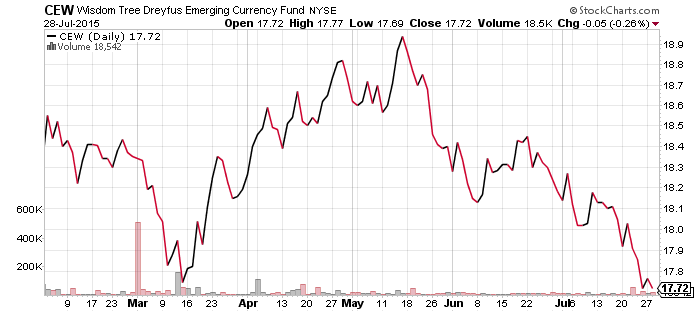

WisdomTree Emerging Market Currency (CEW)

UUP has been in an uptrend since May, which continues to remain intact. On the downside, the $24.60 marks support and $25.60 is upside resistance. The Fed meeting this week could go a long way to determining whether the dollar tests its recent lows or breaks its two month highs.

The euro and yen have been relatively stable, even though Greek stocks remain weak and are a potential risk over the coming month. For now, attention is shifted away from Greece and has been focused on commodities and emerging markets.

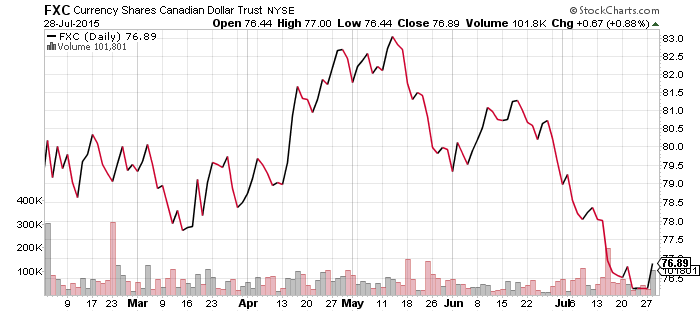

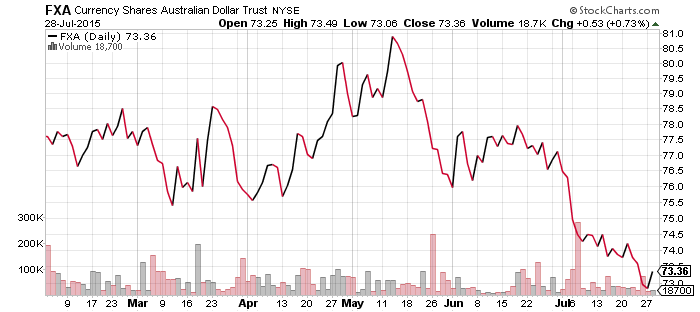

Emerging market currencies were hit by news out of China last week. The government announced the yuan trading band will be widened soon. Each time the band has widened, the yuan has depreciated. The Australian and Canadian dollars both rebounded with commodity prices in recent days, however emerging market currencies kept falling due to China’s announcement.

iShares iBoxx Investment Grade Corporate Bond (LQD)

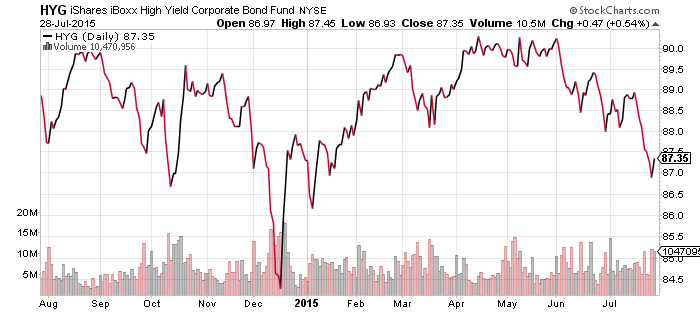

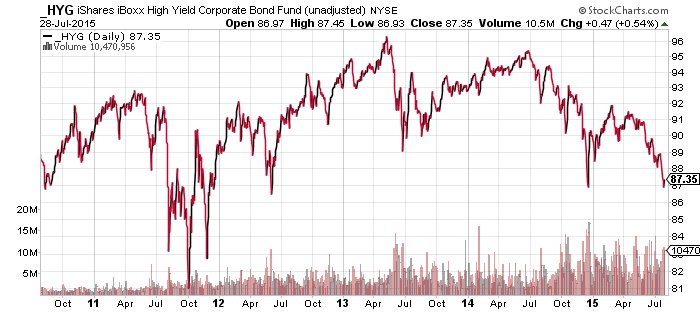

iShares iBoxx High Yield Corporate Bond (HYG)

High yield bonds were pressured by falling oil prices last week. HYG reached the important $87 level this week which marked its lows over the past year. The significance of this level is made clear by a price only chart of HYG, which removes all dividends and looks solely at the NAV of the bonds in the fund. This level also marked a bottom in 2012. Energy prices are the key; if they drop, investors will start to worry about the solvency of shale drillers.

SPDR Utilities (XLU)

SPDR Pharmaceuticals (XPH)

SPDR Materials (XLB)

SPDR Consumer Staples (XLP)

SPDR Consumer Discretionary (XLY)

SPDR Healthcare (XLV)

SPDR Technology (XLK)

SPDR Financials (XLF)

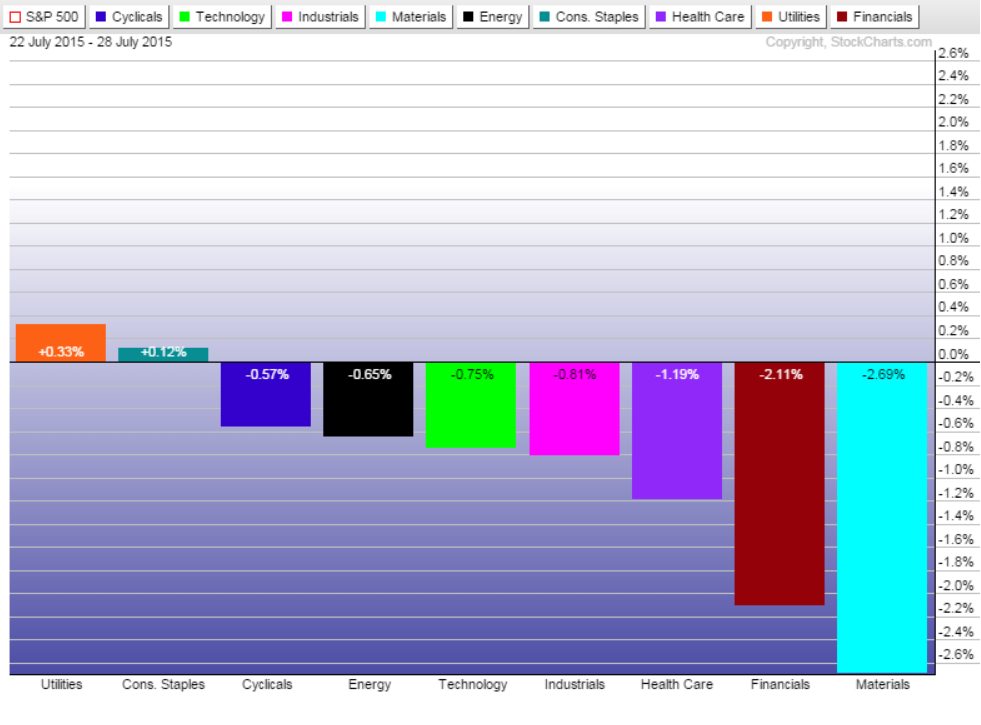

Utilities and consumer staples were the only two winners in a down week for the markets.

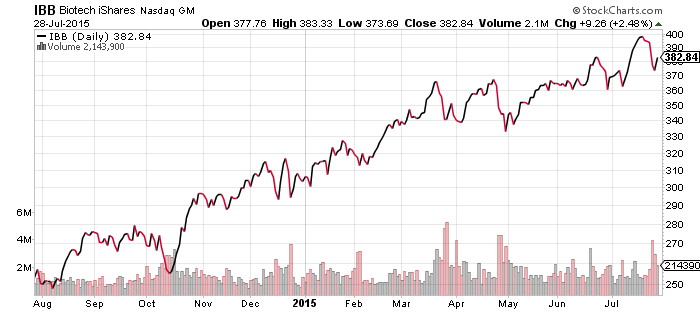

Healthcare care was the third largest loser due to a sell-off in biotechnology. The dip was a healthy one but didn’t push biotechnology below its lows for July. Biogen (BIIB) was responsible for the dip. Its shares fell more than 25 percent on disappointing earnings and drug pipeline news.

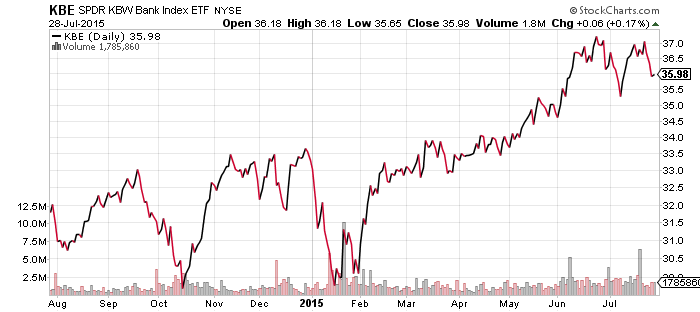

Financial ETFs pulled back as well ahead of the Fed meeting. A dovish statement could hurt financials but in all likelihood, investors have already priced in this possibility.

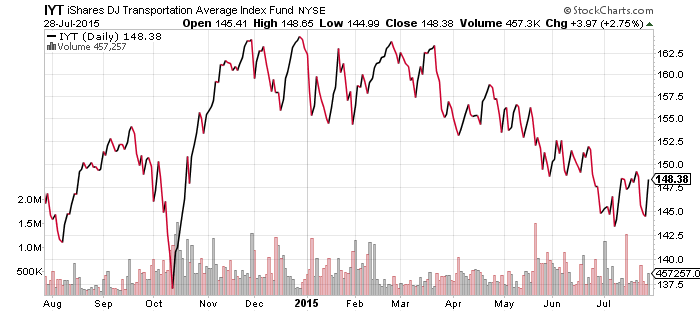

The transports have firmed up and may be turning but it wouldn’t take a lot to push IYT to new lows. Since it is in a bearish pattern since December, caution is still warranted.

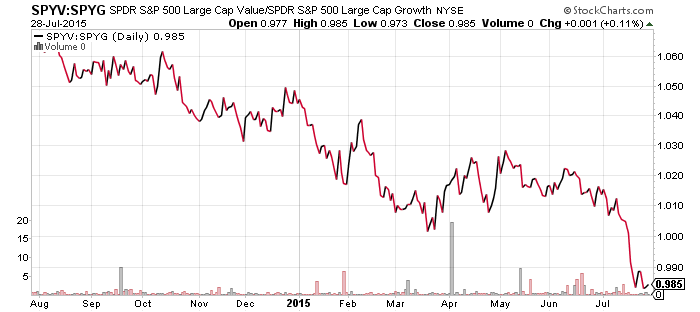

SPDR S&P 500 Large Cap Value (SPYV)

SPDR S&P 500 Large Cap Growth (SPYG)

Energy needs to bottom out or financials need to rally if value is going to end its downtrend.