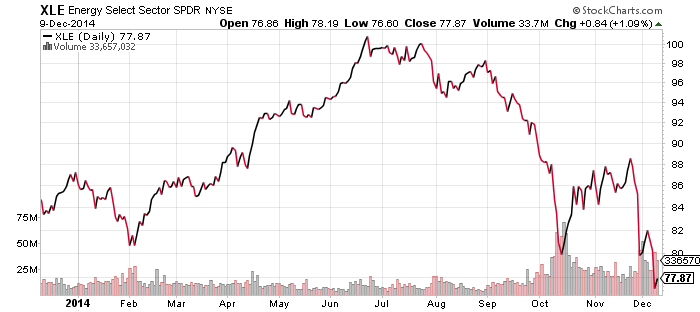

SPDR Energy (XLE)

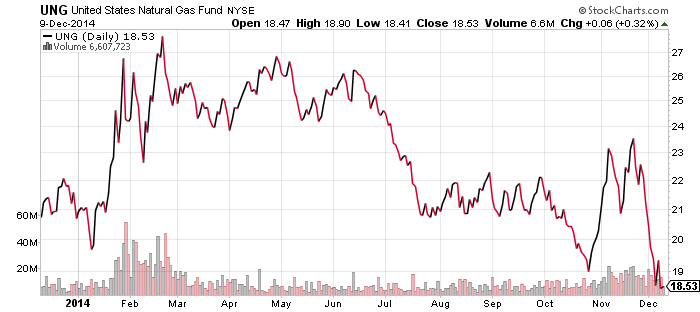

United States Natural Gas (UNG)

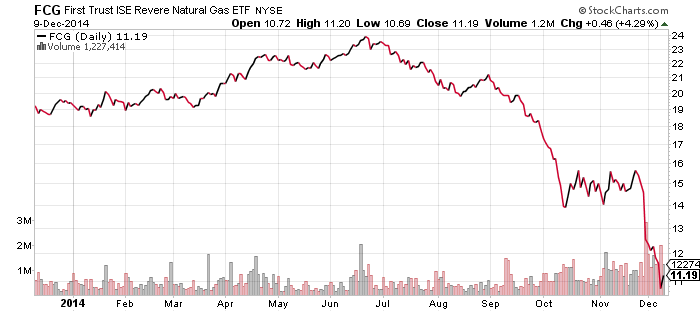

First Trust ISE Revere Natural Gas (FCG)

Global X Nigeria (NGE)

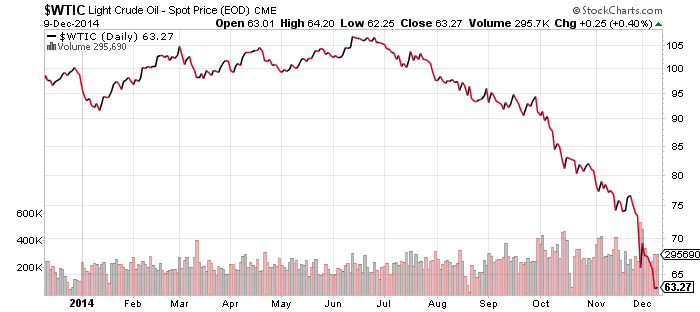

Energy is still the top story dominating the markets. Oil prices are sliding again after failing to stabilize near $65. Today, it was comments by Iran that triggered further selling. The nation said oil could slide to $40 a barrel if OPEC doesn’t work together. Iran also called the falling price “treachery” because geopolitical enemy Saudi Arabia pushed for the current policy. Although Saudi Arabia is hurt by falling oil prices, it is less affected than countries such as Iran, Russia, Nigeria and Venezuela.

Natural gas prices have also turned lower due to warmer weather in December. An extended period of mild weather can alleviate the risk of rising prices in 2015 by giving companies time to build up their inventories. Strong production in Marcellus shale is also weighing on prices.

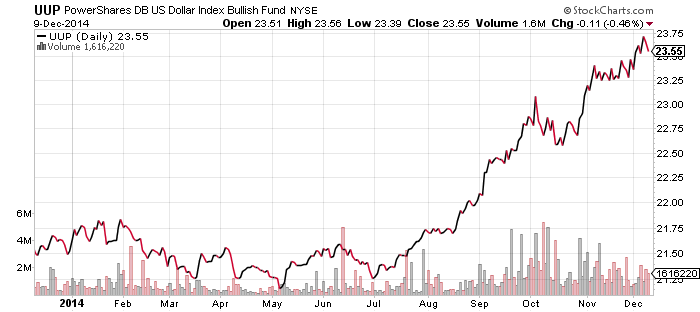

PowerShares U.S. Dollar Index Bullish Fund (UUP)

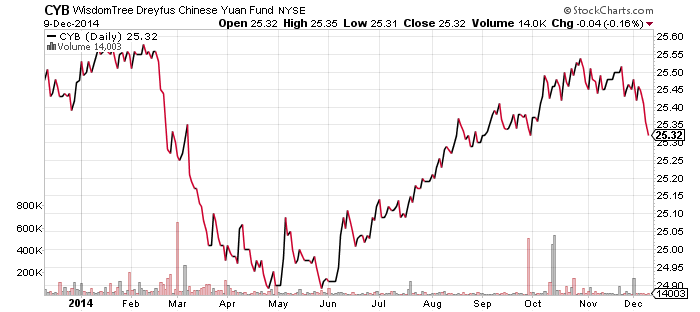

WisdomTree Dreyfus Chinese Yuan (CYB)

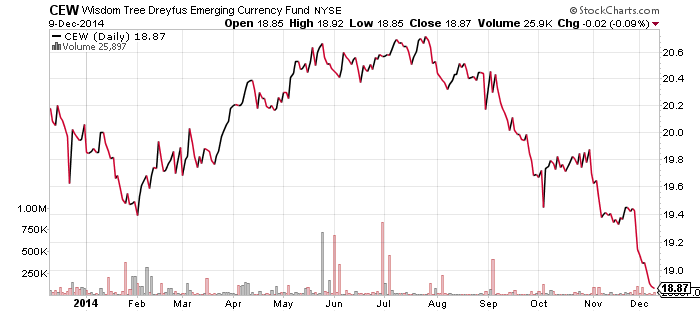

WisdomTree Dreyfus Emerging Currency (CEW)

The U.S. dollar rally took a breather over the past week as measured by the U.S. Dollar Index. The Japanese yen rallied versus the greenback and the euro bounced as well.

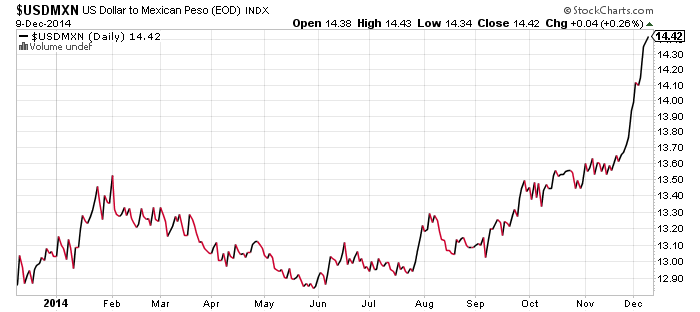

However, the dollar continued to rally against emerging market currencies and oil exporters though. The Mexican government announced it would sell U.S. dollars in order to defend the peso, which has rapidly depreciated since OPEC’s decision to hold production steady. On Monday and Tuesday, China’s yuan also devalued as capital outflows increased in November. Weak trade data also increased expectations for interest rate cuts. Hot money has flowed into China to take advantage of those higher interest rates, but if rates are headed lower, this money may seek a new home.

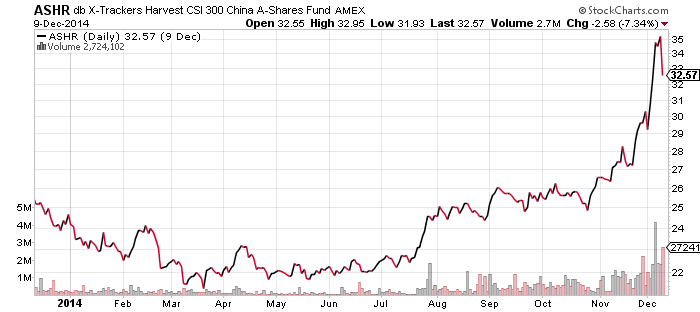

db X-Trackers Harvest CSI 300 A-Shares (ASHR)

China’s incredible A-share rally hit the brakes on Tuesday after regulators tightened credit rules on corporate bonds. Financial institutions can no longer use bonds with low credit ratings for repurchase agreements, which reduces the availability of credit in the financial market. The purpose of the change was to prevent a potential bubble, as the stock market’s swift advance has been fueled by rising leverage. Small investors have also piled into the market over the past couple of weeks, with new accounts surging.

Despite the move of regulators to slow the market, the bull rally is still intact. The drop in the Shanghai Composite erased only a few trading days worth of gains.

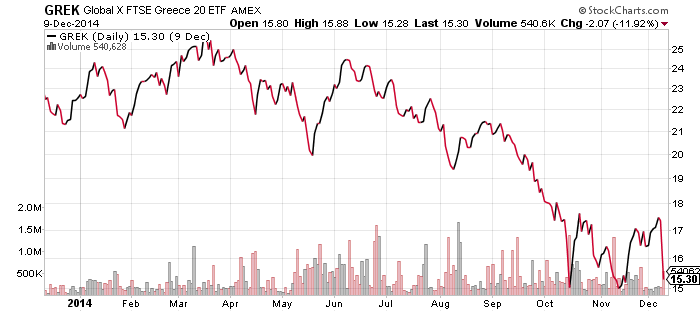

Global X Greece (GREK)

Greece’s stock market saw its biggest plunge since 1987 on Tuesday and bond yields climbed towards their recent highs. The catalyst for the move was the decision to hold a snap presidential election on December 17. Prime Minister Samaras moved the election up in hopes of staving off the rising Syriza party. Should his gambit fail and his candidate lose, an early parliamentary election could follow.

Syriza opposes austerity and has said it would terminate any deals with the European Central Bank or International Monetary Fund. This has investors nervous because a scuttling of the deals could touch off a new panic in Europe.

The chart shows GREK nearing its lows for the year, as it’s unknown which way the vote will go. The way the Greek system works is that members of parliament vote for the president, who needs 200 votes in either the first or second round of the election. The ruling coalition has only 155 seats, so it needs help from smaller parties. If it can’t reach 200 votes in the first two rounds, a third round is held. Only 180 votes are needed to win the third round, but if no one is elected by the third round, a snap parliamentary election is held, which would fall in late January.

Syriza is in favor of the elections because it is rising in the polls. Smaller parties may or may not join with them, depending how they expect to fare in a general election. According to at least one report, odds of a general election are running at about 50/50.

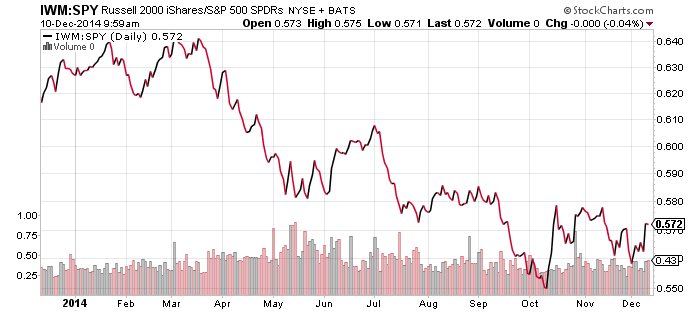

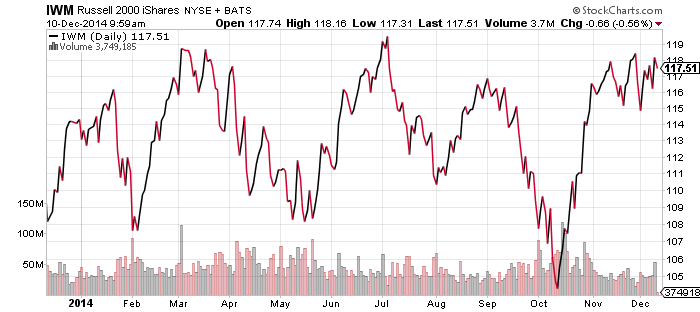

SPDR S&P 500 (SPY)

iShares Russell 2000 (IWM)

The small cap Russell 2000 Index made up some ground versus large cap stocks last week. The index still remains in a sideways trading pattern, but it has been slowly moving in a bullish direction. Small cap stocks gained on Tuesday even though the broader market slipped.

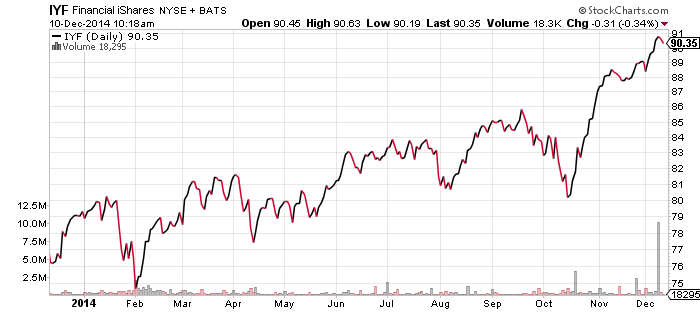

iShares U.S. Financials (IYF)

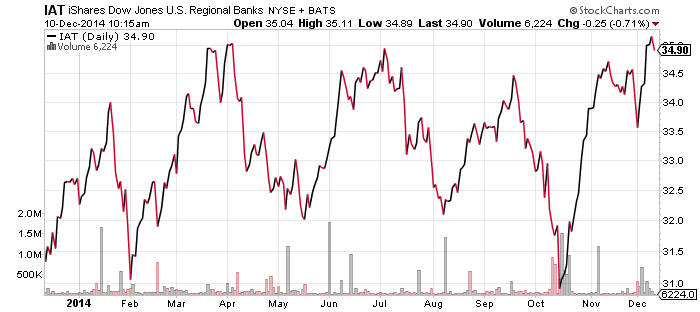

iShares U.S. Regional Banks (IAT)

Financial stocks have been outperforming the S&P 500 Index by a wide margin over the past several weeks and were further boosted by Friday’s strong payroll data. Wage growth was solid too, coming in at 0.4 percent in November.

Strong economic data is increasing expectations for higher interest rates in 2015. This is good news for banks because when rates go up, they also widen, allowing banks to profit more from a growing rate spread between deposits and loans.

Regional banks rely on lending more than larger banks who have trading divisions and investment banking. This has kept share prices down in 2014, but on Friday, the regional bank ETF, IAT, hit a new 52-week high.