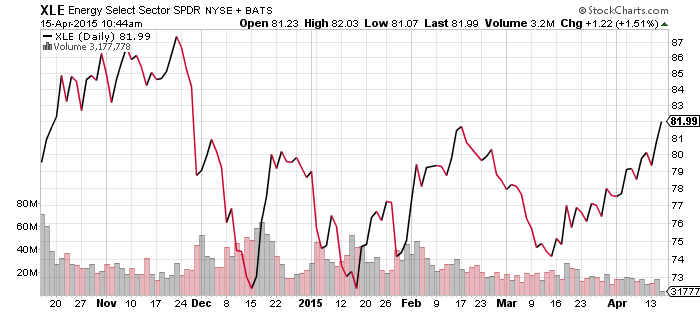

SPDR Energy (XLE)

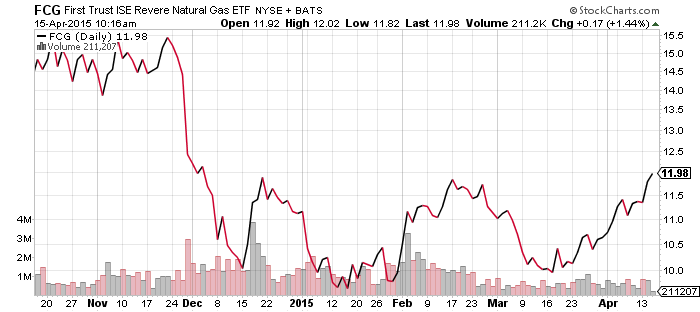

FirstTrust ISE Revere Natural Gas (FCG)

Guggenheim Canadian Energy Income (ENY)

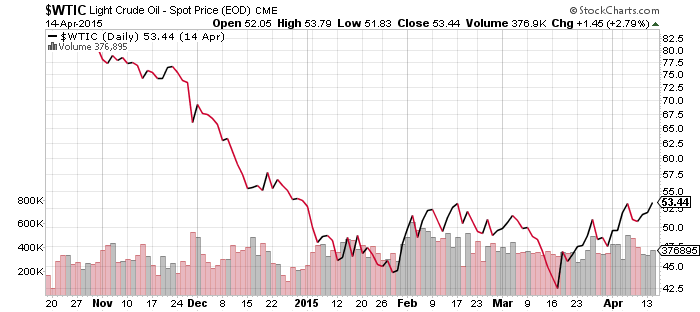

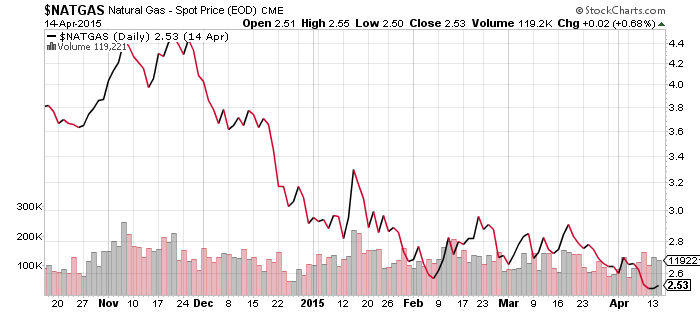

Oil prices have settled into the low $50 range and a positive short-term bullish trend remains in effect. Given the volatility in the oil market and geopolitical risks, this relative calm may be shattered at any moment, but for now, prices are pushing higher. One factor helping the market is that U.S. oil production is either beginning to drop in some areas, or projected to drop by May. This should ease inventory pressure and begin moving the market back towards a balance of supply and demand. The data from last week favors this view: oil inventory grew at a much slower pace.

Energy remains key for the stock market because weakness in this sector is why large-cap stocks have only gained about 2 percent since November. XLE is challenging its February high today and a push higher will open up a move towards the November levels. If that happens, the broader stock market will rally.

SPDR Utilities (XLU)

SPDR Pharmaceuticals (XPH)

SPDR Materials (XLB)

SPDR Consumer Staples (XLP)

SPDR Consumer Discretionary (XLY)

SPDR Healthcare (XLV)

SPDR Technology (XLK)

SPDR Financials (XLF)

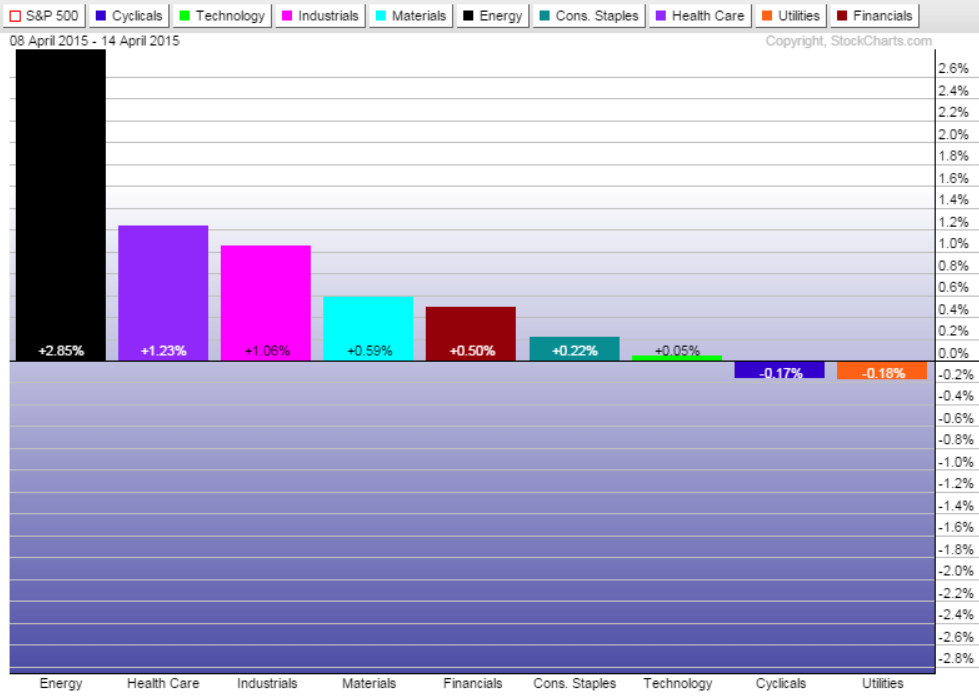

Energy was the best performing sector over the past week, more than doubling the return of healthcare stocks. The worst performers were utilities and consumer cyclicals, which were down less than 0.2 percent.

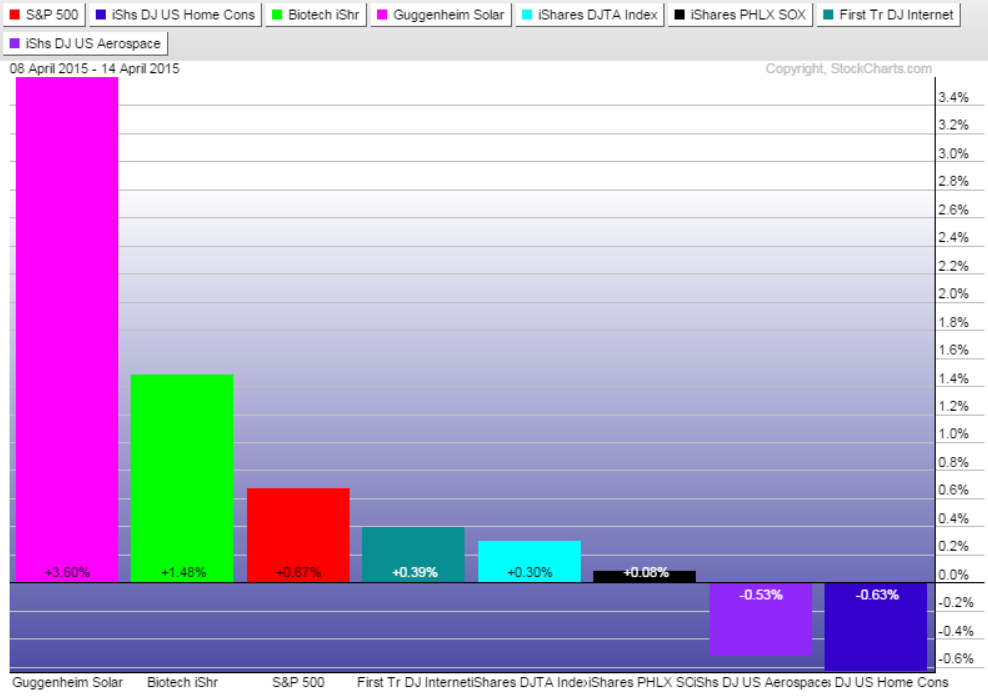

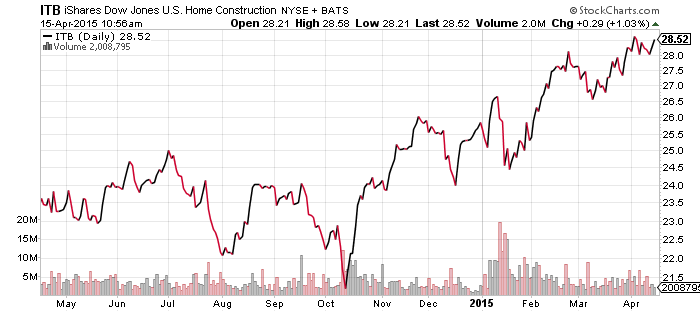

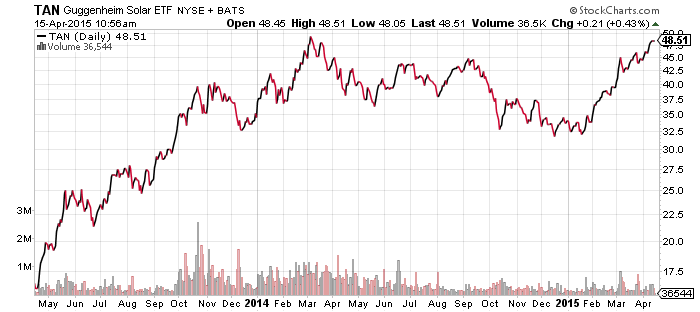

Among sub-sectors, solar remains strong and biotech continues to pull the healthcare sector higher. Internet funds were slowed by the EU filing a complaint against Google (GOOG). Homebuilder confidence climbed to its highest level in almost a year in this month, allowing homebuilder ETFs to be on the verge of a new 52-week high.

Guggenheim Solar (TAN)

TAN is approaching its 2014 high. We had expected a correction in recent weeks because interest rates continue to fall, which typically leads to weaker performance in solar stock. If TAN doesn’t correct soon and continues on the current trajectory, it will make a new multi-year high a possibility. It would then open up a challenge of the $70-plus highs from 2011, about a 40 percent move from current levels.

PowerShares U.S. Dollar Index Bullish Fund (UUP)

CurrencyShares Euro Trust (FXE)

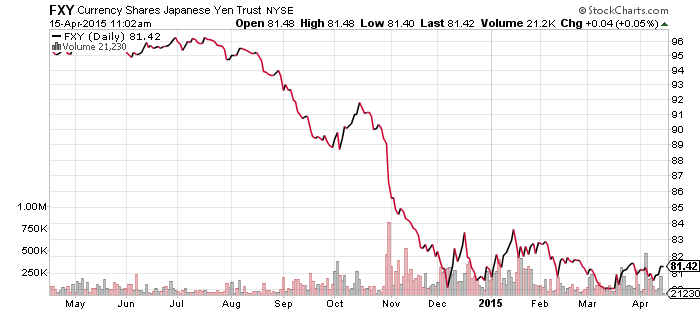

CurrencyShares Japanese Yen (FXY)

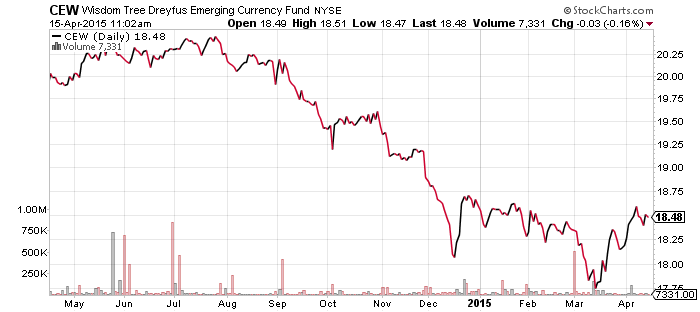

WisdomTree Dreyfus Emerging Currency (CEW)

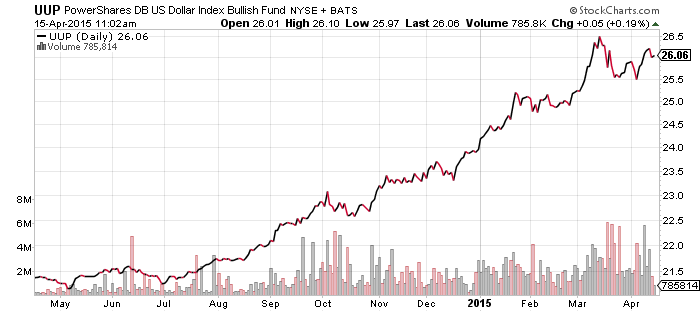

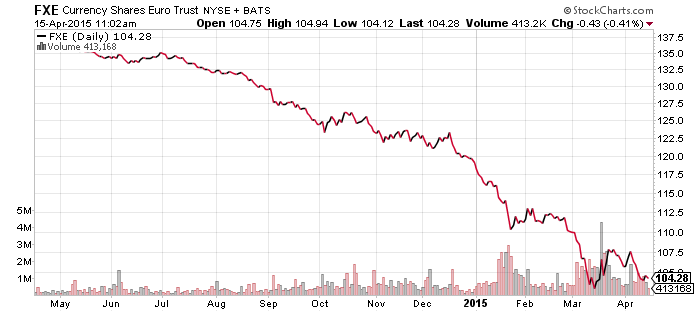

The big story in the currency markets this week was a rumor that the Greek government is preparing to default on an IMF loan. This sent the euro back near its lows for the year, before recovering. Although the Greek government denied the rumor, it will continue to hang over the market. The euro has been in a range between $1.05 and $1.10 since hitting its lows and it’s likely to remain at those levels until the latest Greek situation is resolved.

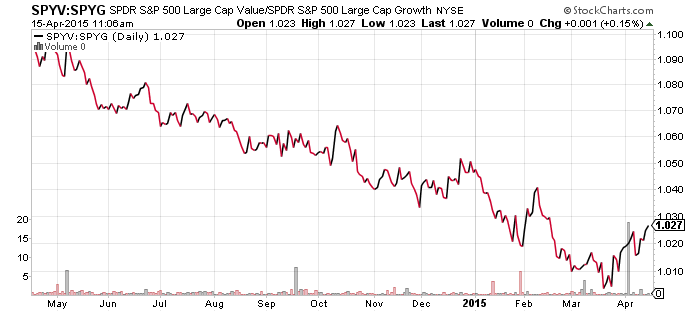

SPDR S&P 500 Large Cap Value (SPYV)

SPDR S&P 500 Large Cap Growth (SPYG)

Value stocks have rebounded strongly since late March, aided by the rally in energy. It’s still too early to say if a significant shift is underway, but a trend is intact. Value stocks represents a good opportunity relative to growth, given that is has underperformed for almost the entirety of the post-2008 bull market.

The key sectors for value are financials, energy, telecom and utilities. For growth, it is technology, healthcare and consumer discretionary. In terms of relative exposure, technology, financials and consumer discretionary are the sectors that will have the largest impact on the relative price of SPYV versus SPYG.

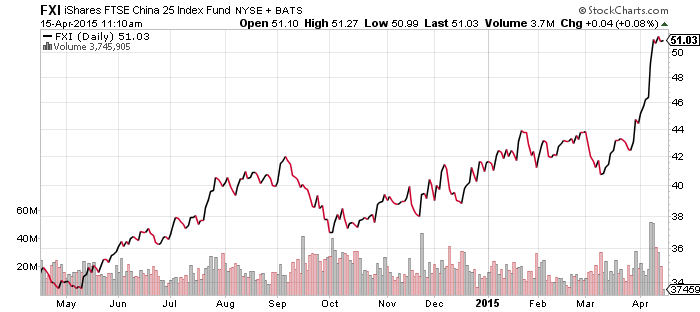

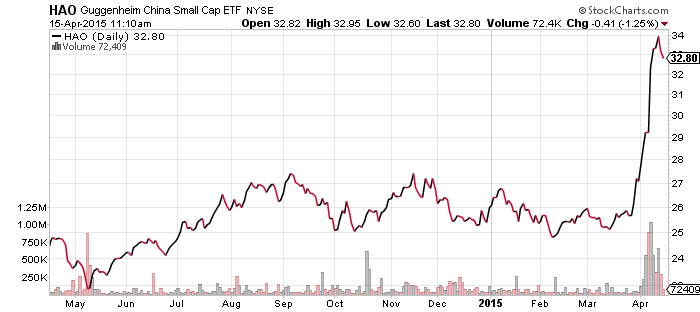

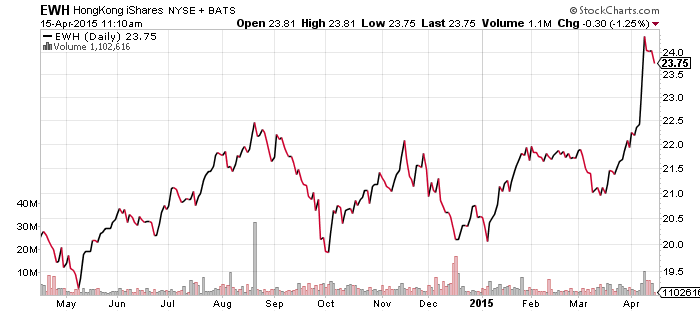

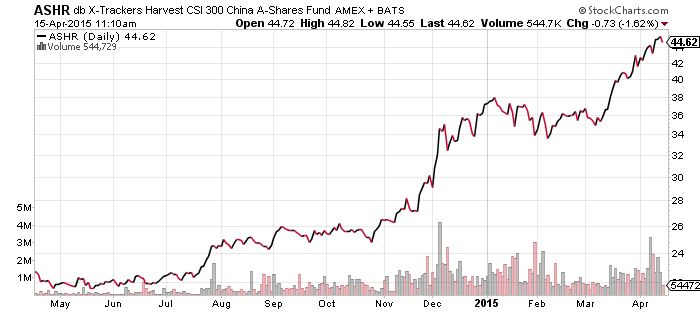

iShares MSCI Hong Kong (EWH)

Guggenheim Small Cap China (HAO)

iShares China Large Cap (FXI)

db X-Trackers China A Shares (ASHR)

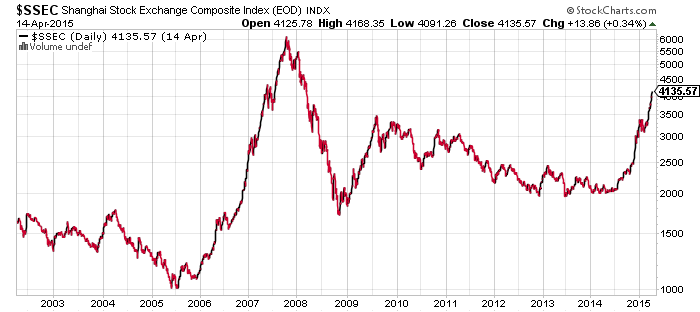

The surge in Hong Kong traded shares finally took a pause. The Chinese A-share market remains in a steady uptrend and has gained more than 100 percent over the past nine months. Volume on the Shanghai exchange now regularly exceeds the levels seen at the 2007 peak, when the Shanghai Composite crossed 6000. Going solely by the volume and the growth in the economy, a move to new all-time highs is not hard to imagine. It also only took the Shanghai Composite a little more than 2 years to go from 1000 to 6000, a 600 percent advance, so the current pace of the advance has precedent.

China’s market is dominated by retail investors, which is why it is more prone to booms and busts. Psychology plays a larger role and most participants in the market are traders looking to sell shares at higher prices, not investors evaluating company fundamentals. Right now investors are pouring into the market and new investors are the fuel for higher prices. When they stop opening new accounts or psychology shifts, the same stampede into the market that carried it higher, will cause devastating losses for those who stay too long.