SPDR Utilities (XLU)

SPDR Pharmaceuticals (XPH)

SPDR Materials (XLB)

SPDR Consumer Staples (XLP)

SPDR Consumer Discretionary (XLY)

SPDR Healthcare (XLV)

SPDR Technology (XLK)

SPDR Financials (XLF)

With the timely close of the quarter, we’ll start off this week looking at sector performance, and a broader review of the first quarter.

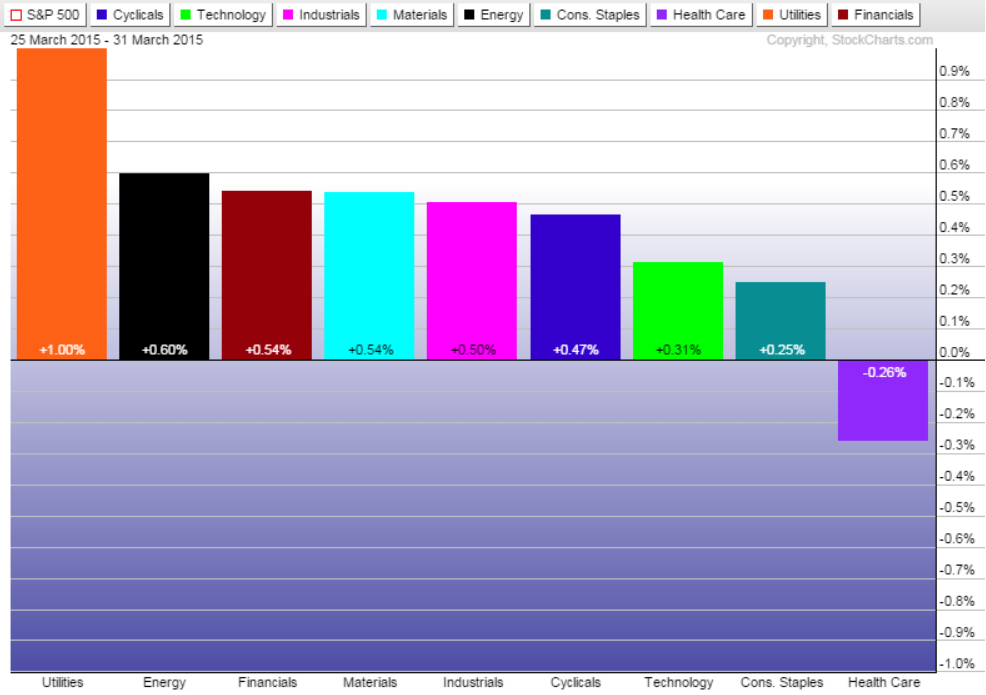

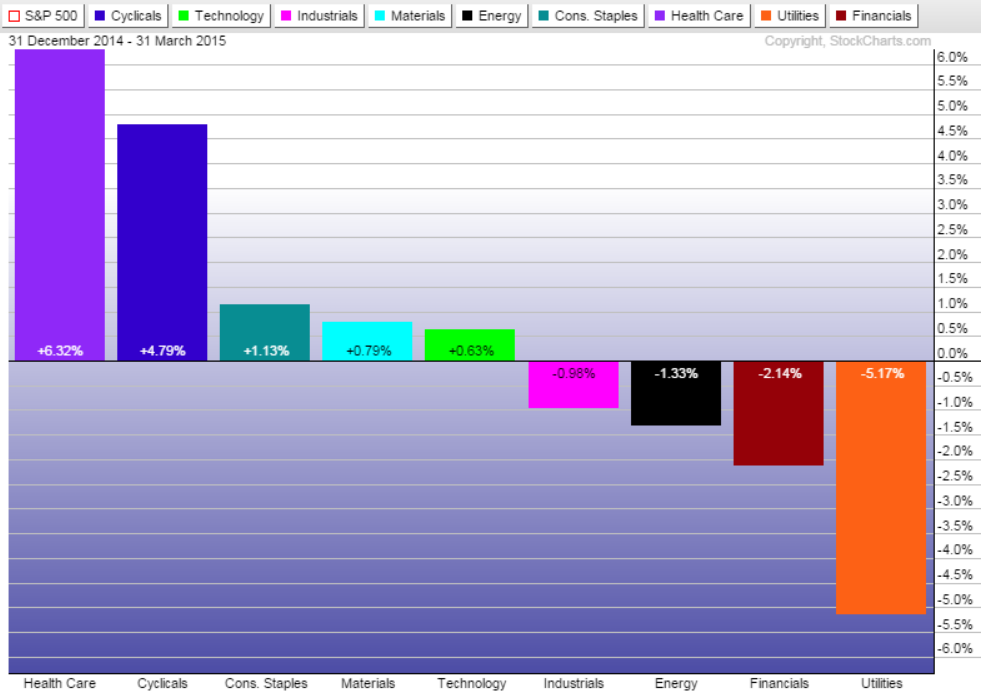

Last week, utilities led the market after interest rates slid lower. However, energy and financials, two of the worst performing sectors in 2015, also rallied. Healthcare, a top performer so far this year, declined on the week after biotechnology stocks sold off.

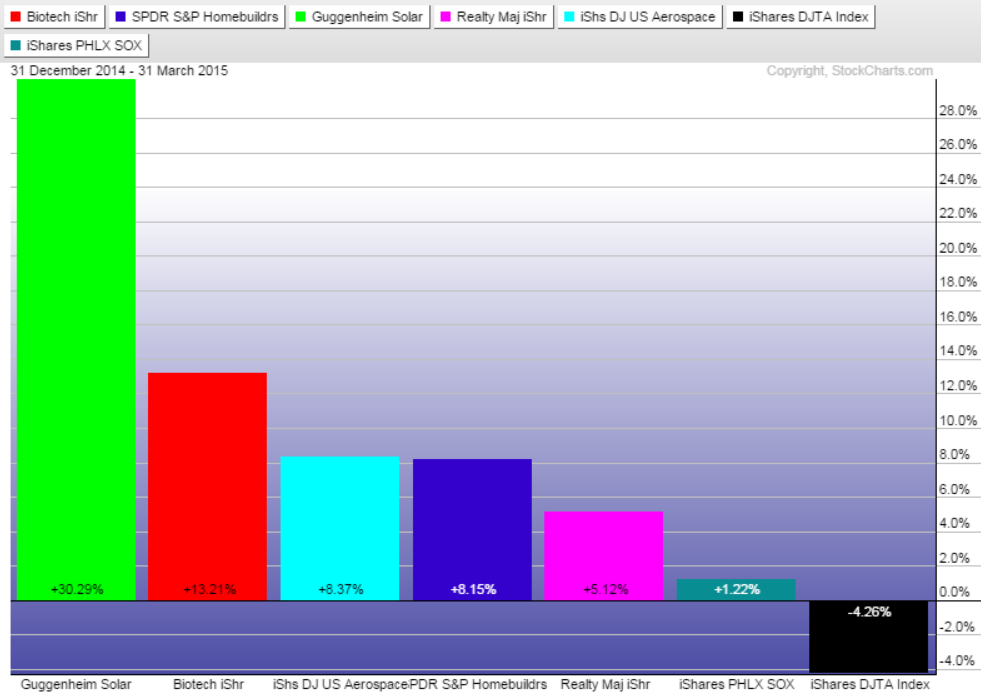

Among the subsectors, Guggenheim Solar (TAN) beat the market by a wide margin, rallying more than 30 percent. Biotechnology saw its gains trimmed by last week’s decline but finished the quarter with double-digit gains. Home builders and aerospace/defense were two of the better performing subsectors. Transportation sold off over the past few days as stubbornly low oil prices are starting to impact earnings of railroad firms. IYT is down 4 percent on the year.

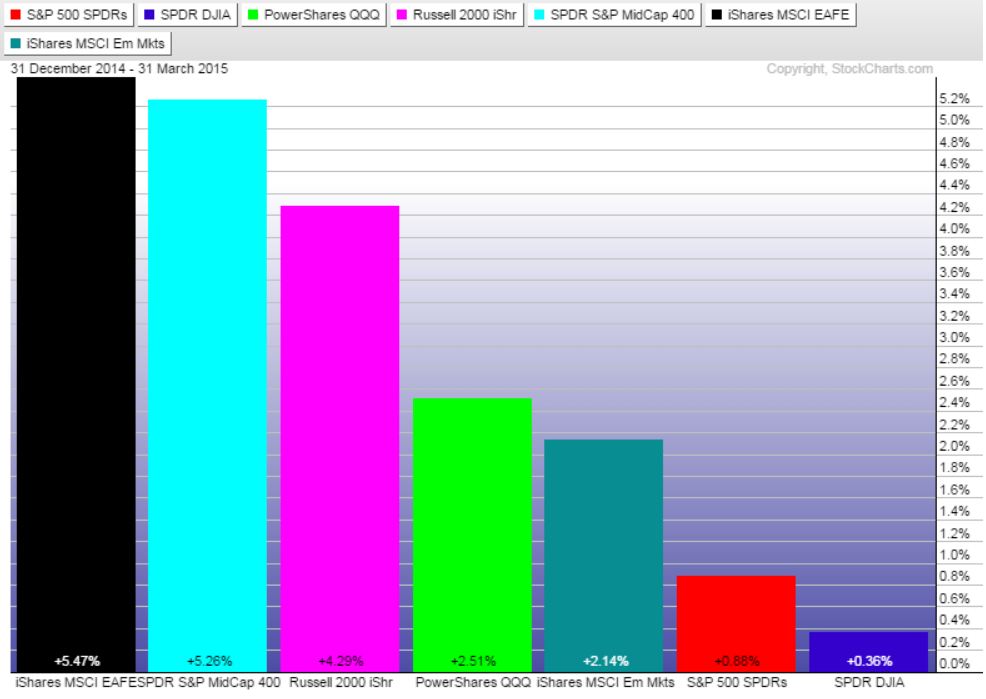

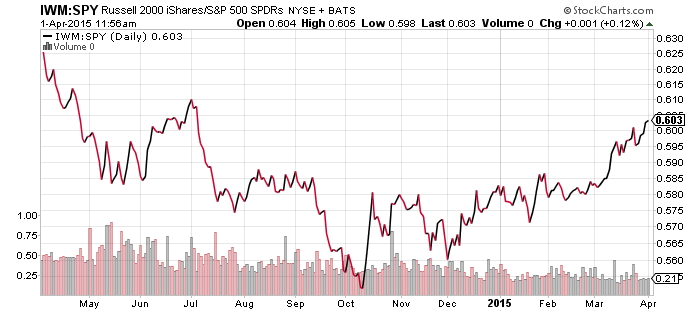

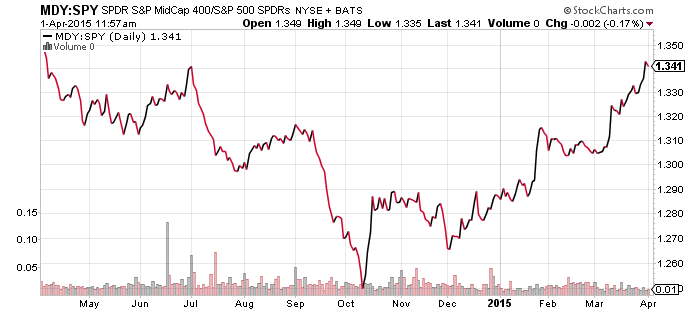

The MSCI EAFE was the best performing major index, as quantitative easing fueled a stock rally in Europe. In the U.S., mid- and small-caps beat the broader market by a wide margin. Aside from making up for lost ground in 2014, one theory is that these stocks are outperforming due to investors avoiding multinationals in found the S&P 500 Index because their earnings and revenues are hurt by the strong dollar.

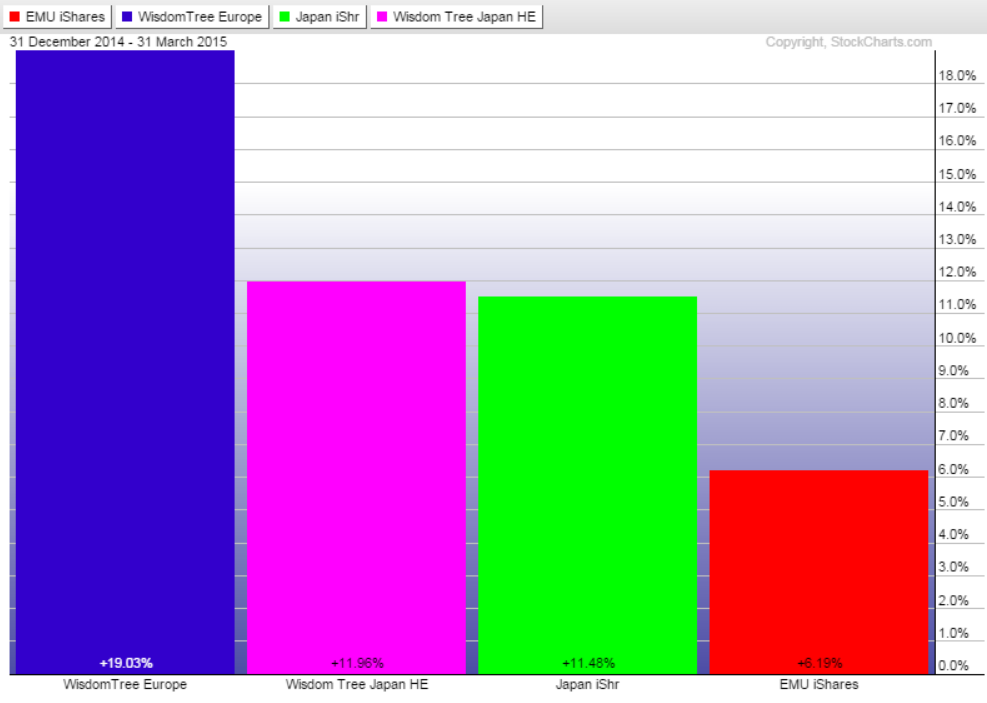

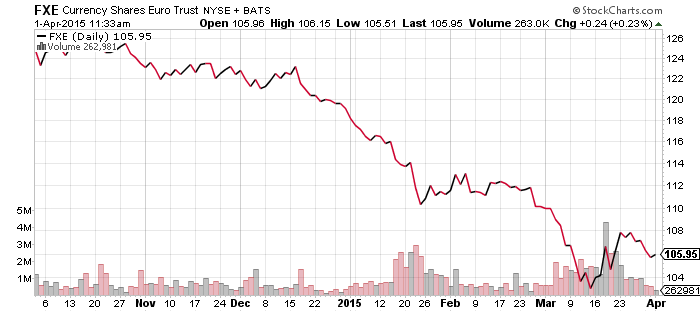

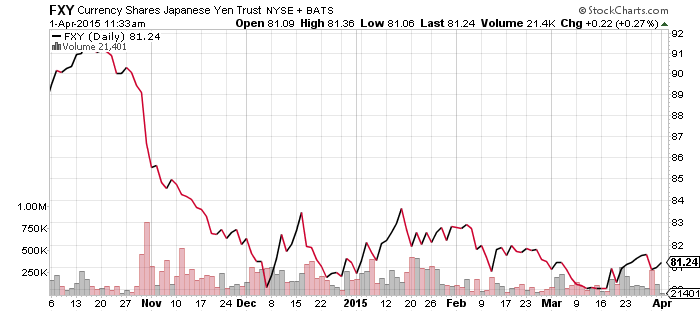

Although the MSCI EAFE did well, investors who hedged their currency exposure did far better. iShares EMU Index (EZU) gained 6.19 percent in the first quarter, but WisdomTree Europe Hedged (HEDJ) rallied 19.03 percent thanks to avoiding losses in the depreciating euro. With the yen relatively flat this year, hedged and unhedged Japan ETFs delivered similar results.

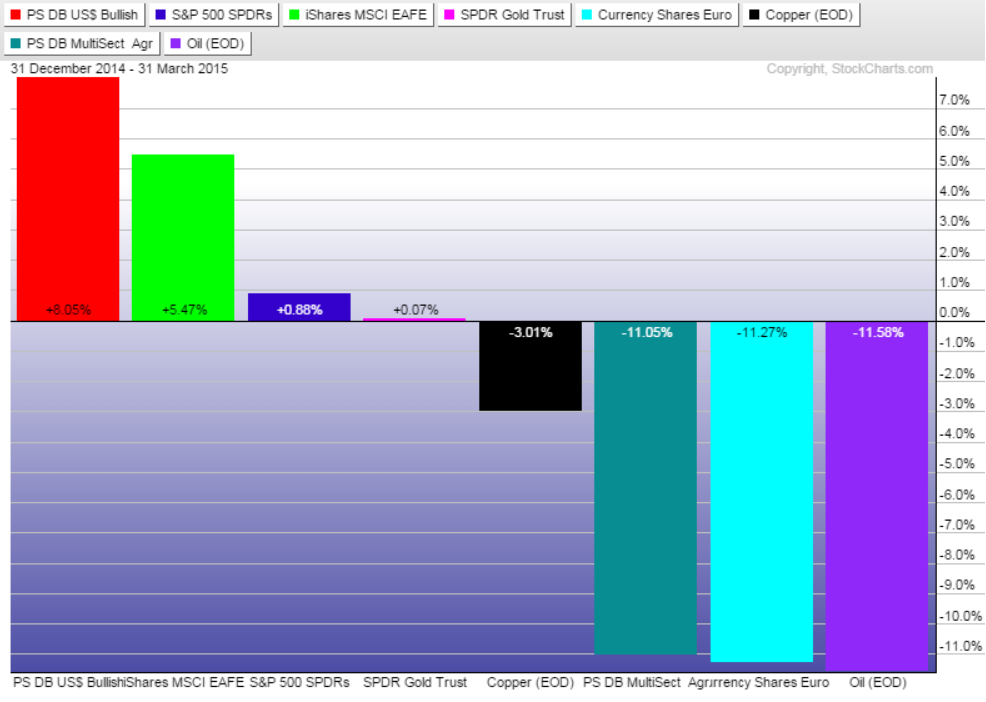

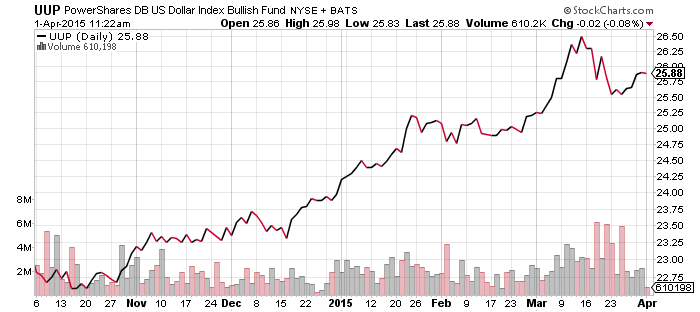

The easiest trade to make in the first quarter was to buy PowerShares U.S. Dollar Index Bullish (UUP). UUP’s 8 percent advance beat most major indexes. A correction may already be underway but the dollar remains in a bull market. Oil, the euro and agricultural commodities were among the worst performing assets, with copper also declining by 3 percent. Gold was basically flat, a strong performance considering the U.S. dollar rally.

PowerShares U.S. Dollar Index Bullish Fund (UUP)

CurrencyShares Euro Trust (FXE)

CurrencyShares Japanese Yen (FXY)

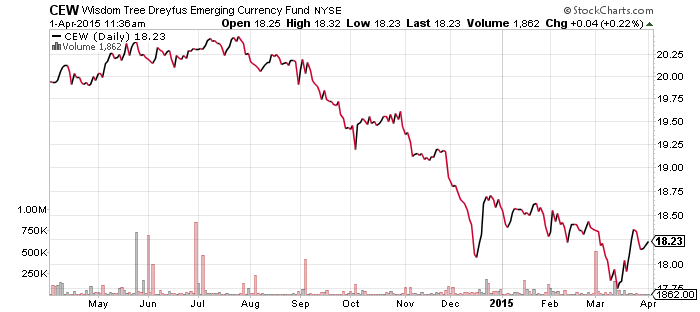

WisdomTree Dreyfus Emerging Currency (CEW)

UUP rallied over the past week as the euro corrected from its rebound. ADP’s employment report was below expectations, which sent the dollar lower and gold higher.

FXY remains relatively flat, but economic weakness in Japan has been working to strengthen the yen. If global equity markets were to sell-off, the yen would likely rally, otherwise it may remain range bound.

CEW remains in a downtrend and it needs to climb above the resistance line shown in the chart below for it to have a short-term bullish outlook. As the second chart of CEW shows, the pace of the long-term decline in CEW is slowing and a turnaround looks increasingly likely, at least for the short-term. A rebound would coincide with euro strength.

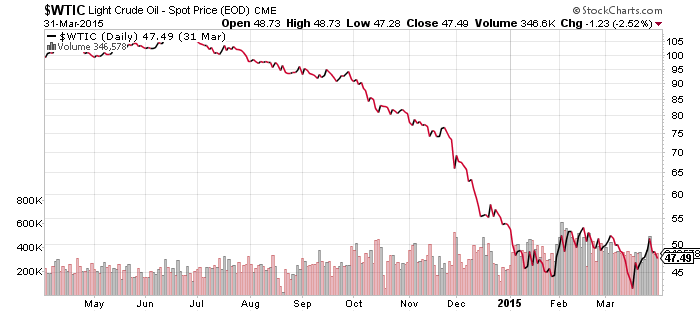

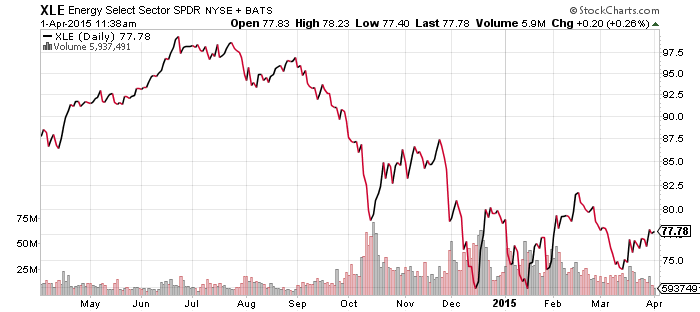

SPDR Energy (XLE)

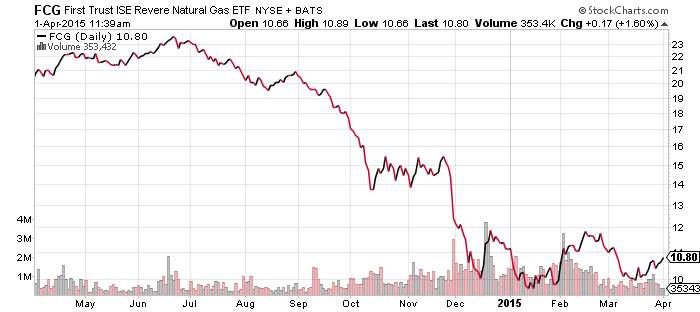

FirstTrust ISE Revere Natural Gas (FCG)

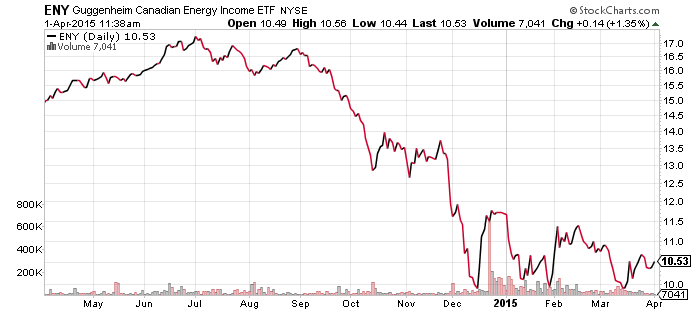

Guggenheim Canadian Energy Income (ENY)

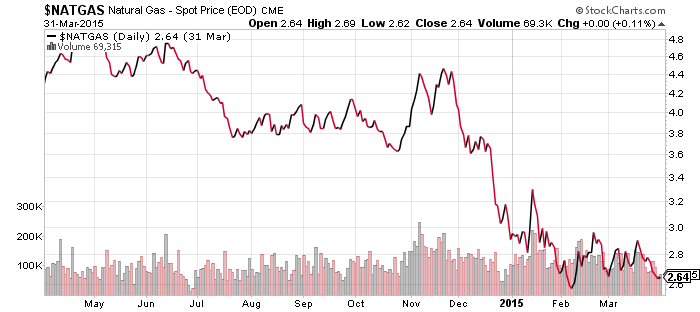

Inventory continued to build last week, even though oil production declined for the second time in 2015. Oil prices finished lower because they were working off a geopolitical induced rally. Prices briefly climbed above $50 in the wake of Saudi Arabia’s attacks on Yemeni rebels. Putting pressure on prices is the potential nuclear deal with Iran, which could bring more production onto the world market. With the market experiencing surpluses already, more production could further push prices lower. It may be that prices are being held low because speculators anticipate a lifting of sanctions will send oil prices lower, in which case prices might rise following a deal as these speculators cover their short positions.

SPDR S&P 500 (SPY)

iShares Russell 2000 (IWM)

S&P Midcap 400 (MDY)

PowerShares QQQ (QQQ)

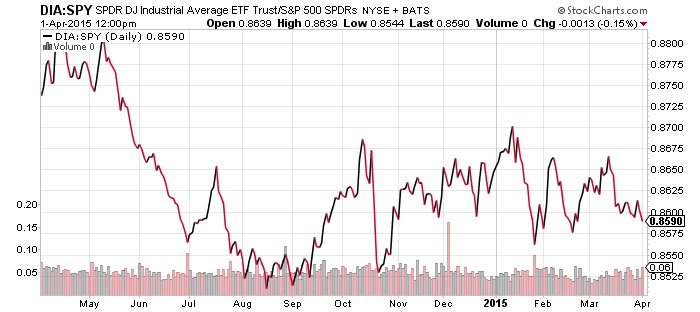

SPDR DJIA (DIA)

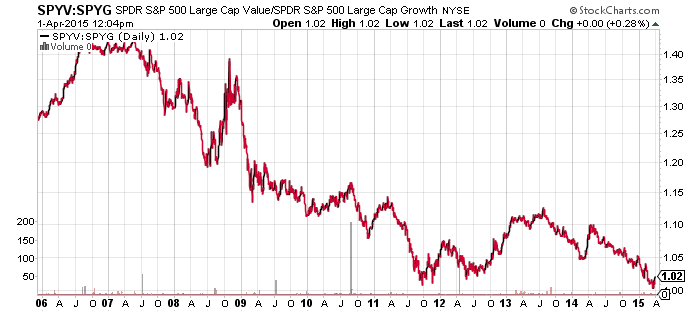

SPDR S&P 500 Large Cap Value (SPYV)

SPDR S&P 500 Large Cap Growth (SPYG)

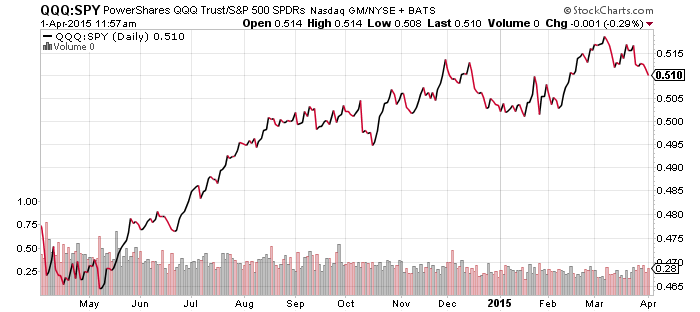

Small-caps led again last week, and mid-caps beat large caps as well. The technology and biotech heavy Nasdaq trailed, due to the sell-off in biotech and semiconductor stocks. QQQ has been underperforming SPY for nearly a month. Technology is the most export reliant sector in the S&P 500 Index and while advanced technology companies tend to see more stable demand for their products, the strong dollar may finally be taking a toll on the sector.

The Dow continues to lag the S&P 500 Index. Large-caps are underperforming and the Dow has a higher average market capitalization than the S&P 500, $175 billion versus $132 billion.

Value stocks are also outperforming now, but the trendline shows the value sector has a ways to go before it breaks the previous downtrend. A rebound similar to 2014 could occur if the market sells off and pulls growth shares lower. Longer term, growth has led since the previous market top in 2007, but value may have completed a double bottom having successfully retested the 2011 price ratio low.

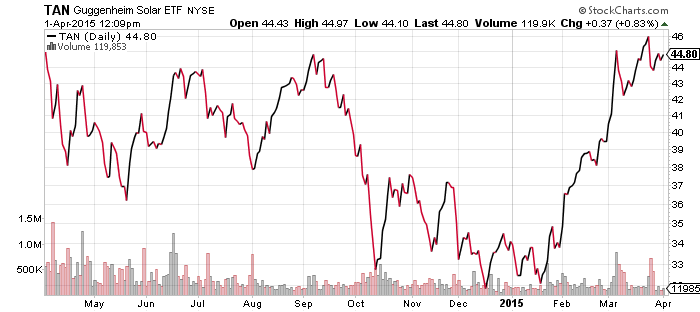

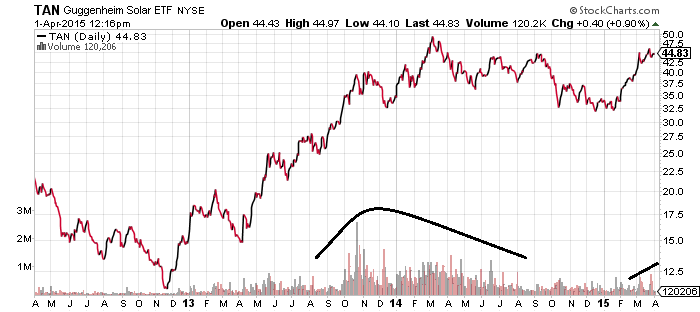

Guggenheim Solar (TAN)

Interest rates have been falling and it appears investors are taking some risk off the table. A correction in the solar sector is therefore likely. A decline of as much as 10-15 percent is possible in the short-term, but a drop to that level would not violate the recent bullish breakout.

Longer term, TAN needs to break above $50 to signal a major bullish breakout. Notice the volume in TAN increased greatly in late 2013 and into 2014, which coincided with the rally to $50. Since then volume has declined. The recent breakout was accompanied by higher volume and that volume must be sustained if TAN is to break the 2014 high.