SPDR S&P 500 (SPY)

SPDR DJIA (DIA)

PowerShares QQQ (QQQ)

Fidelity Contrafund (FCNTX)

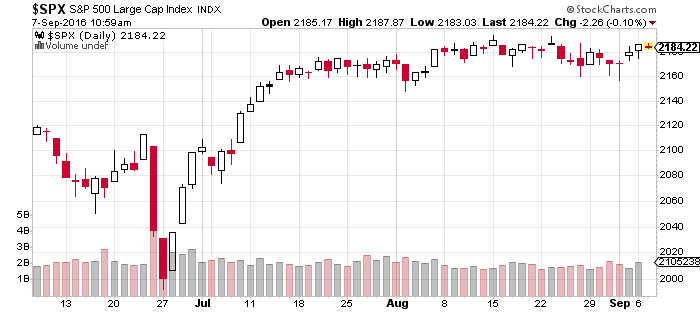

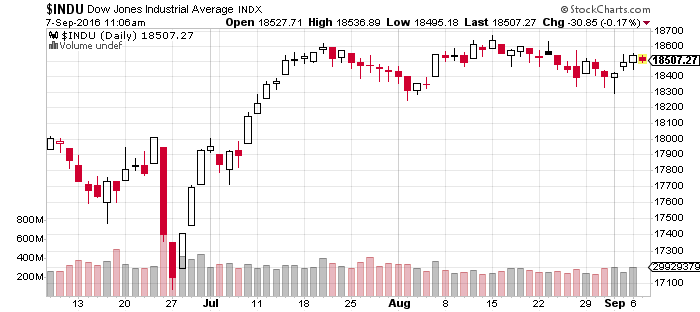

The S&P 500 Index and the Dow Jones have remained in narrow trading ranges as traders ease back into post-holiday market.

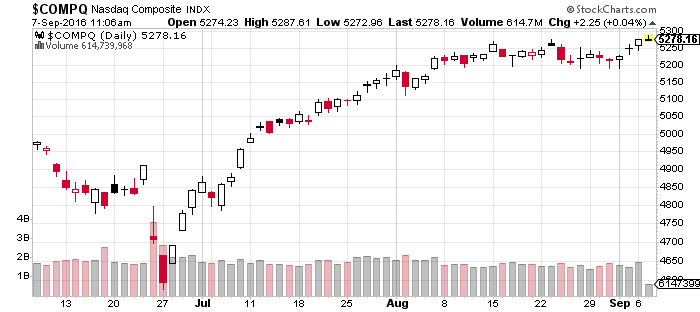

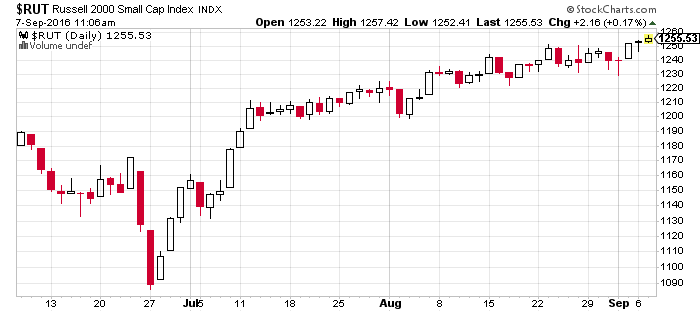

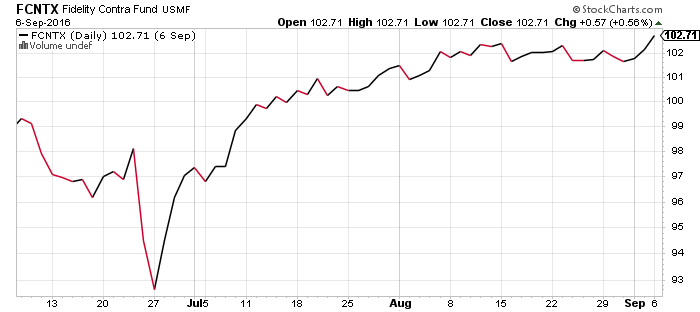

The Nasdaq and Russell 2000 Index, however, have moved to new 52-week highs over the past week. Fidelity Contrafund (FCNTX) followed the Nasdaq to a new 52-week high.

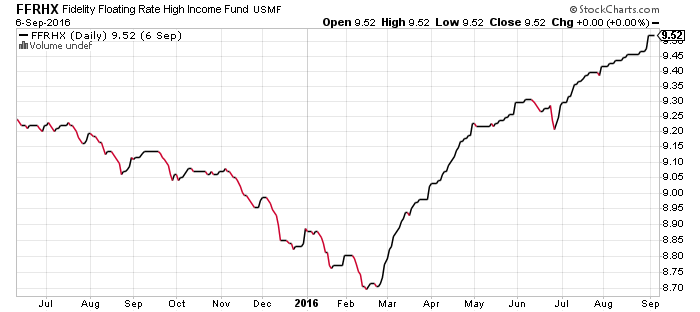

Fidelity Floating Rate High Income (FFRHX)

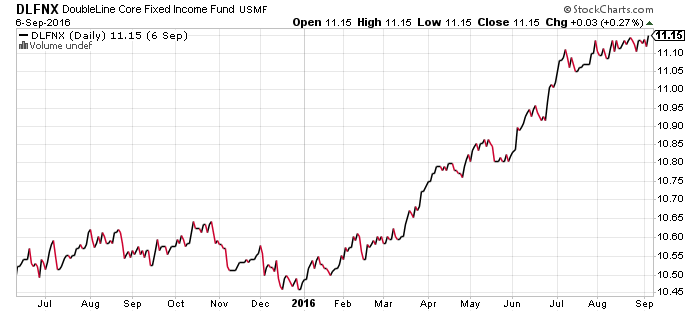

DoubleLine Core Fixed Income (DLFNX)

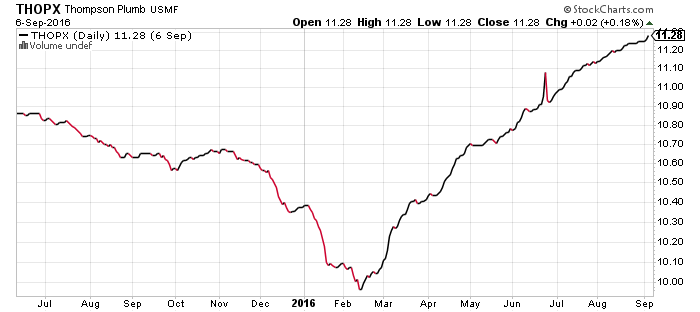

Thompson Bond (THOPX)

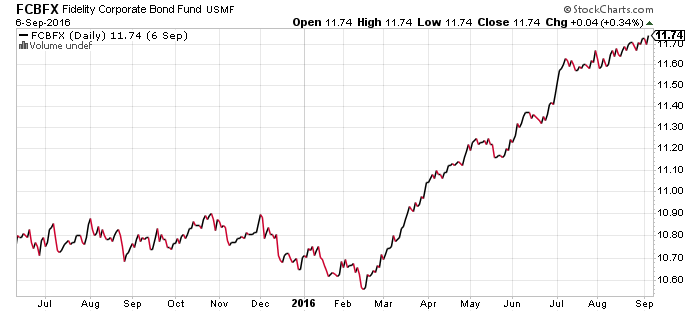

Fidelity Corporate Bond (FCBFX)

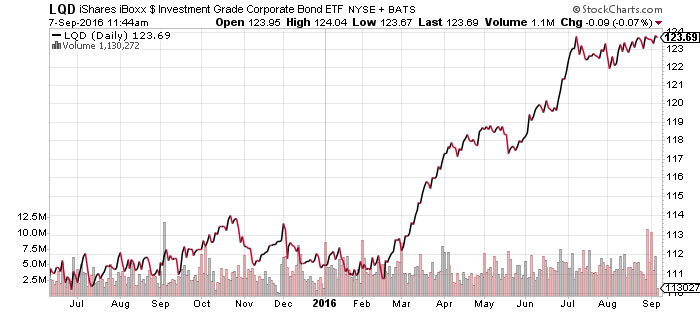

iShares iBoxx Investment Grade Bond (LQD)

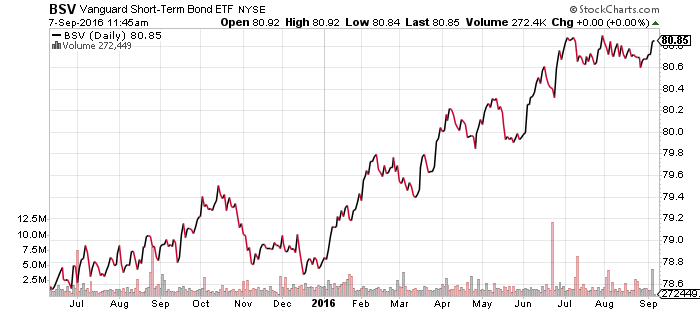

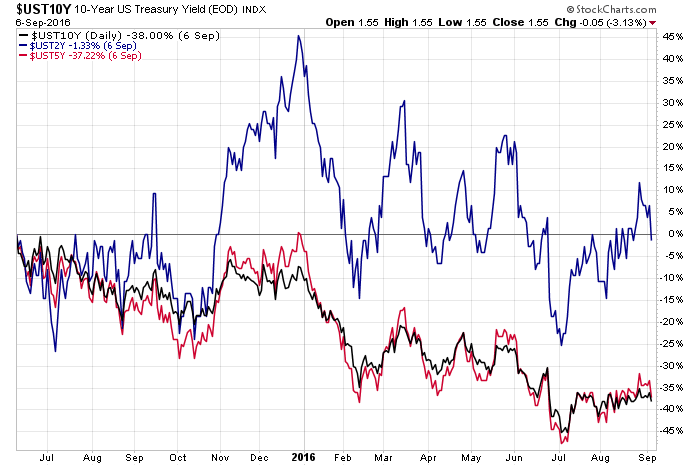

Treasury yields fell following slightly weaker-than-expected labor market data. The Federal Reserve’s Labor Market Conditions Index effectively quashed chatter calling for a September rate hike, sending bonds higher on Tuesday. July’s Job Openings and Labor Turnover Survey (JOLTS) was released on Wednesday and beat expectations with a spike in openings to offset Tuesday’s report.

Bonds rallied broadly following the JOLTS. Fidelity Corporate Bond (FCBFX), Thompson Bond (THOPX) and Fidelity Floating Rate High Income (FFRHX) pushed to new highs, while LQD is on the verge of a breakout.

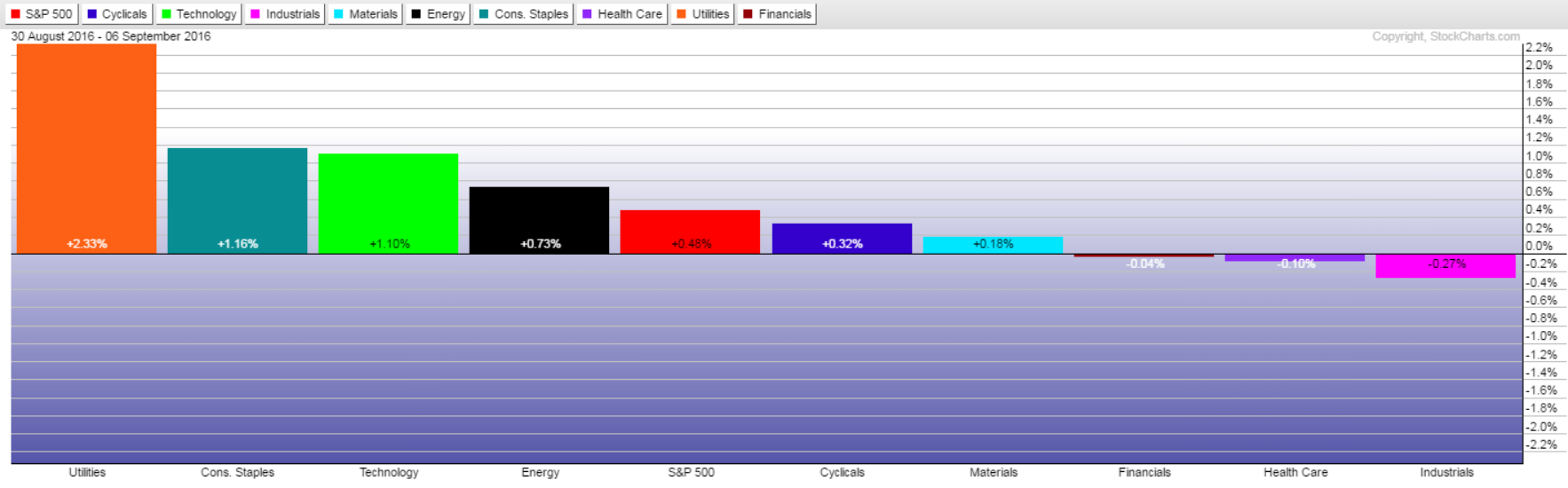

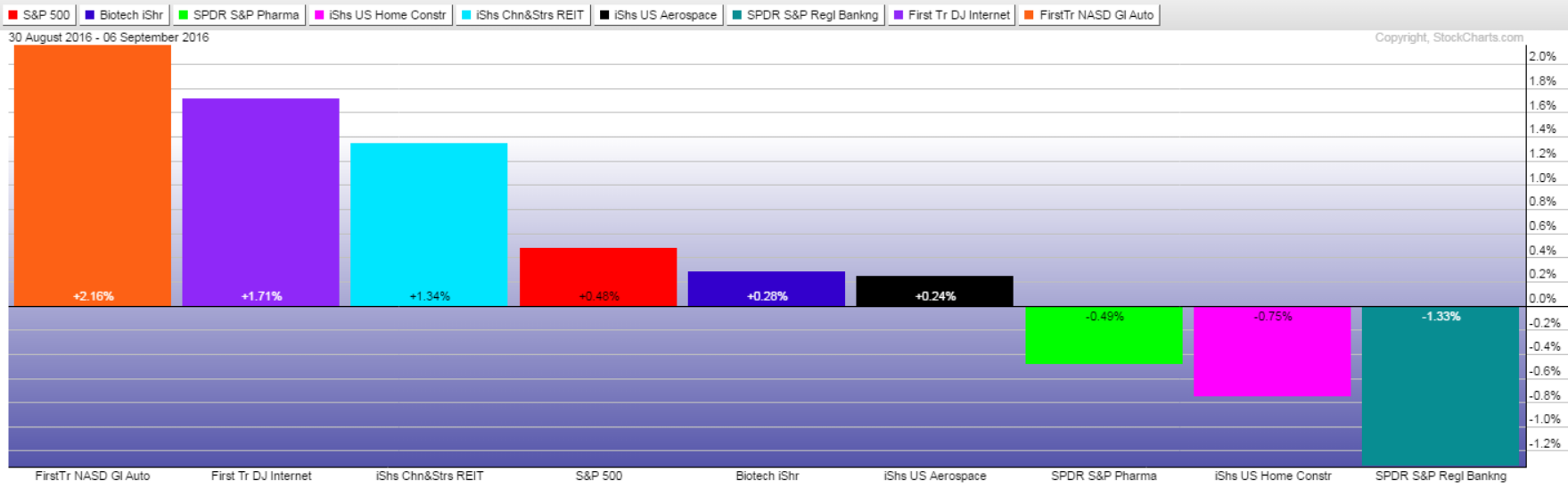

Sector Performance

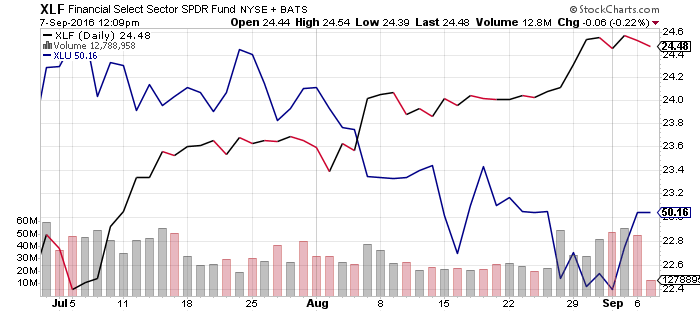

The market’s recent tight ranges brought about predictably modest reversals. The utilities sector rallied more than 2 percent as rate hike odds declined, while financials waivered slightly as investors priced in the probability of a December increase.

Although auto sales missed optimistic forecasts in August, higher margin SUVs and crossover vehicles increased their market share. Auto stocks rallied as a result.

The Internet subsector lifted the Nasdaq to new 52-week highs as reflected in the performance of FirstTrust Dow Jones Internet (FDN).

The rate-sensitive real estate sector followed utilities higher over the past week, while home construction and regional banks declined with market interest rates.

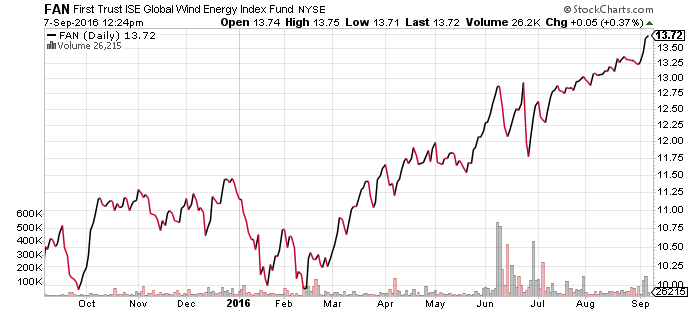

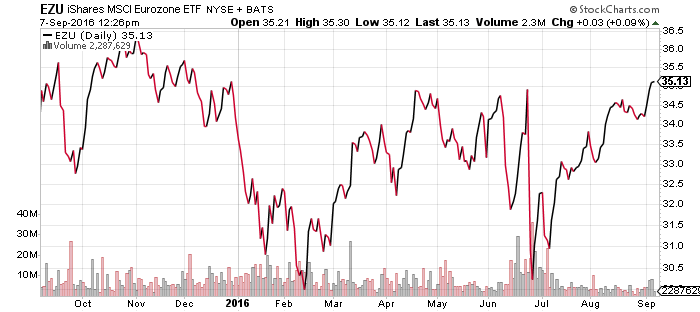

FirstTrust ISE Global Wind (FAN) spiked over the past week due primarily to a bounce in European shares, as reflected in iShares MSCI Eurozone (EZU). The European Central Bank will announce its latest interest rate policy on Thursday.

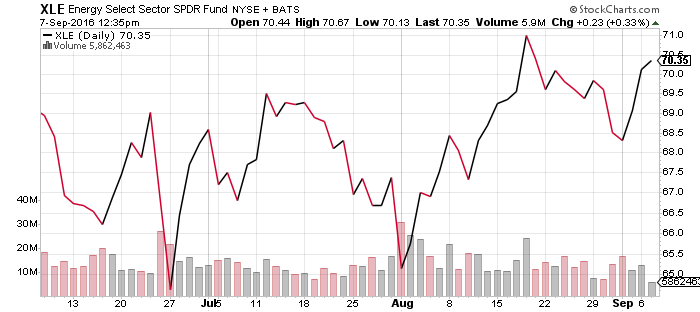

SPDR Energy (XLE)

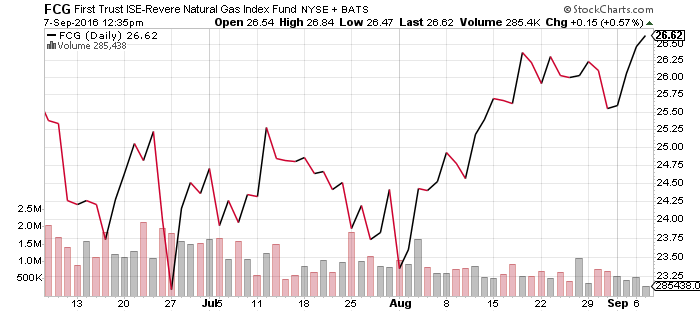

First Trust ISE-Revere Natural Gas (FCG)

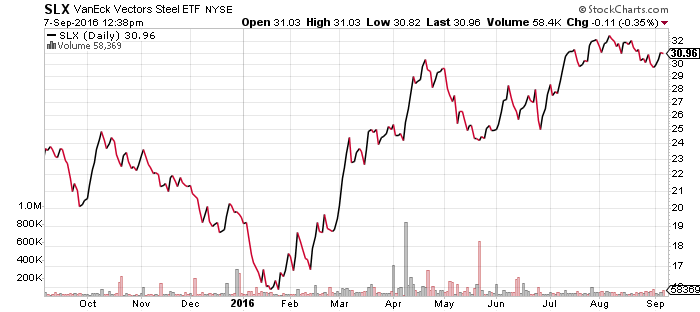

Market Vectors Steel (SLX)

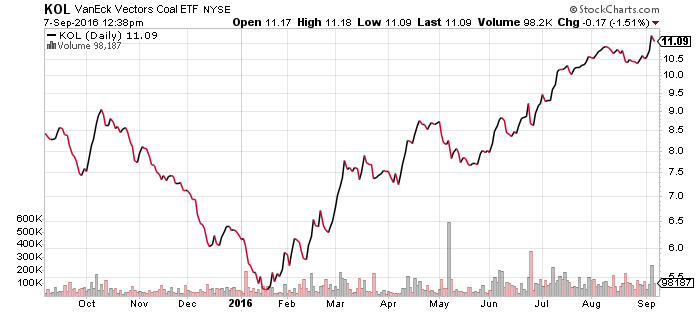

Market Vectors Coal (KOL)

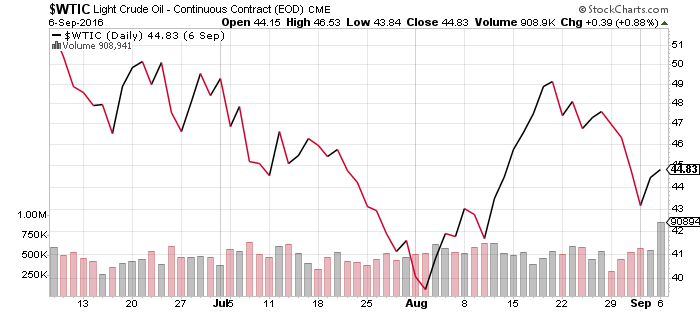

West Texas Intermediate Crude fell over the past week. News of a production cut agreement between Russia and Saudi Arabia sent prices higher on Monday while U.S. markets were closed. The agreement merely called for stabilization, however, leading to a quick reversal as details emerged.

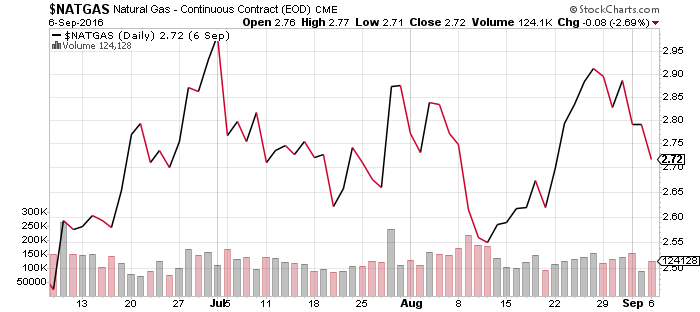

Natural gas traded lower during the week, but shares of gas producers bounced. FCG is trading at its highest level in 2016.

KOL also rallied to a new 52-week high. A flurry of economic data from China could factor into commodity prices over the coming weeks.

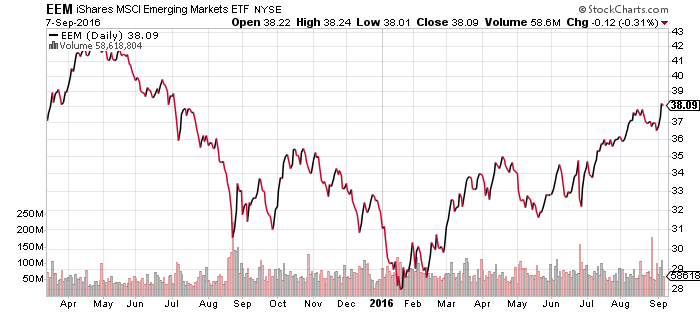

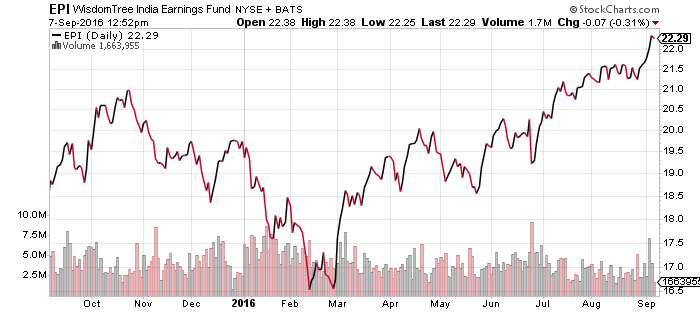

iShares MSCI Emerging Markets (EEM)

EEM broke out to a new 52-week high last week. All four of the BRICs pushed higher, led by Indian stocks.

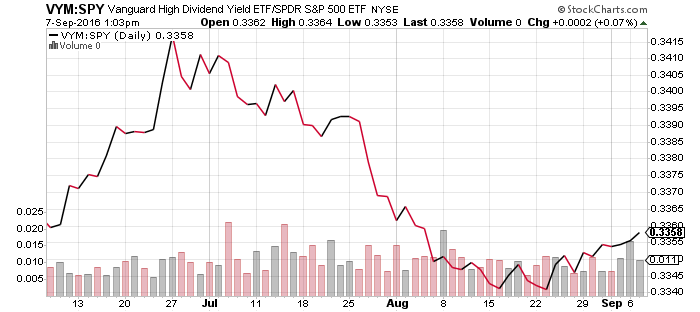

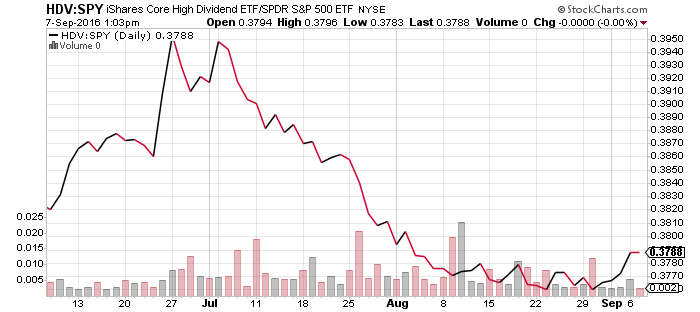

Vanguard High Dividend Yield (VYM)

iShares Core High Dividend (HDV)

Both VYM and HDV started outperforming the S&P 500 Index in late August. Dividend funds should extend short-term uptrends as rate expectations remain low.